Equities moved higher this week as the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite all notched new record highs. Small caps equities lagged. Bond yields fell causing the Barclays Aggregate Bond Index to outpace the S&P 500 on the week. Rhetoric regarding the China-U.S. trade deal is not looking good. China and the United States were supposed to have already signed a Phase 1 deal by now, but headlines read they only agree to continued communications. Leaks are much more suggestive of talks breaking down versus concluding with a deal. On top of this, President Trump met with Federal Reserve Chair Jerome Powell this week. Some may be inclined to put two and two together. The U.S. Legislature passed a bill aiming to protect human rights in Hong Kong. President Trump is expected to sign the bill, which is thought to be a clear negative regarding trade talks with China. The result is China becoming increasingly dismayed with what it perceives as interference by the United States within Hong Kong. These headlines continue to pound the tape and stocks pop and drop with each regurgitation.

Under the surface, the rosy Q3 GDP has waned as the Federal Reserve Bank of Atlanta GDPNow is forecasting a growth of just 0.4% based on available data. These nowcasts are very noisy and while the low number is nothing too significant, it might have more relevance when equities sit at all-time highs. Retail sales remained solid this week as did building permits, which continue to benefit from falling interest rates.

The Federal Reserve released minutes this week from their October meeting. The two key items are conflicting in nature. On the one hand, the minutes emphasized data would need to change materially before enacting further interest rate cuts. On the other hand, officials continue to acknowledge the need to permanently put in place liquidity arrangements to maintain or even increase reserves in the system. This second point gets to the heart of whether a stealth quantitative easing (QE) is underway. At this point it appears as though enough market participants have concluded such action is indeed a QE-type of event. Therefore, this is deemed to be a tailwind to equities and other risk assets, especially when communicated the size and scope are open to further increases in the future.

|

|

Contributed by | Justin Carley, CFA, Managing Director

Justin is a Managing Director, providing portfolio management and credit analysis for fixed income strategies. He also manages the firm’s multi-manager portfolio strategies and contributes to the asset allocation framework. Justin has more than 10 years of experience focusing on management, analysis and trading of fixed income portfolios. Previously, Justin was a fixed income portfolio manager at American Trust & Savings Bank. Justin has a bachelor’s degree from Truman State University, holds the Chartered Financial Analyst designation and holds a Fellowship in the Life Insurance Management Institute.

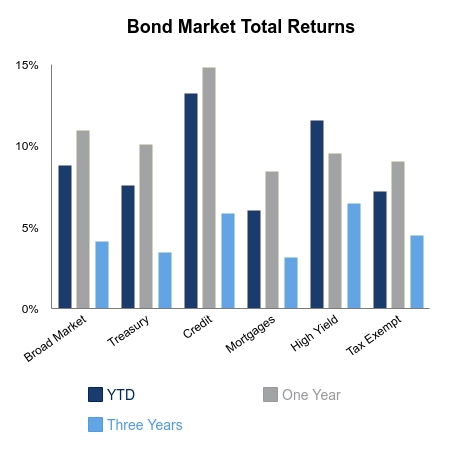

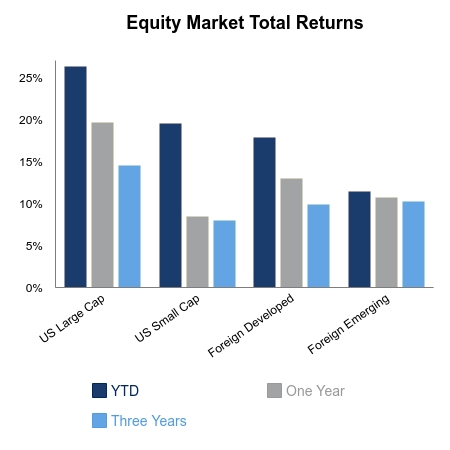

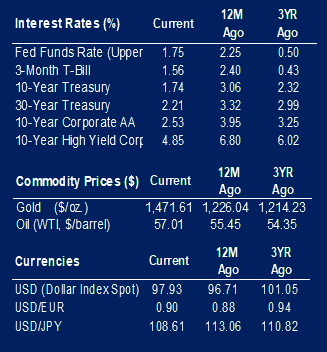

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.