The preliminary GDP numbers for the second quarter were released this week. The decline in the quarter was adjusted from 32.9% to 31.7%. A 1% adjustment in GDP growth used to cause panic among economists. However, the magnitude of the initial decline is so large that people barely blinked with the adjustment.

Personal consumption expenditure (PCE) grew by 1.9% in July. Consensus expectation was for growth of 1.5%. The growth was led by an $82.1 billion increase in spending on goods, led by new vehicle purchases. Spending for services grew by $121.2 billion, led by increases in healthcare and food services spending.

The PCE deflator, the Federal Reserve’s preferred inflation measure, came in as expected at 1% year-over-year. Core PCE, which excludes food and energy, was higher than the expected 1.2% at 1.3%.

Personal income was also higher than expected with growth of 0.4%. The expectation was for a decline of 0.3%. The increases came from the economy reopening and many reentering the workforce. An increase in rental income contributed to the increase. The growth was offset by a scaling back of government social benefits.

Manufacturing strength continued in August. The ISM Manufacturing number for the month was 56. This compares favorably with the expectation of 54.5 and the previous month’s reading of 54.2. The Markit PMI Manufacturing number of 53.1 for the period was also positive, despite coming in slightly below the expectation o 53.6. The Markit and ISM indices are diffusion indices. Anything over 50 is considered positive. The Kansas City Fed Manufacturing Index’s reading of 14 was significantly higher than the expected 2.

July’s durable goods orders final numbers were slightly better than initially reported. Growth was adjusted upward to 11.4% from 11.2%. The growth was led by orders for transportation equipment, up 35.6%. Factory orders were also adjusted up from 5.8% to 6.4% for July.

The strength in housing continued with a pending home sales number of 5.9% for July. This month-over-month reading is higher than the expected 4.4%.

Spending on construction was relatively flat in July at 0.10%. This is lower than the expected growth of 1%, but better than the previous month’s decline of 0.48%.

|

|

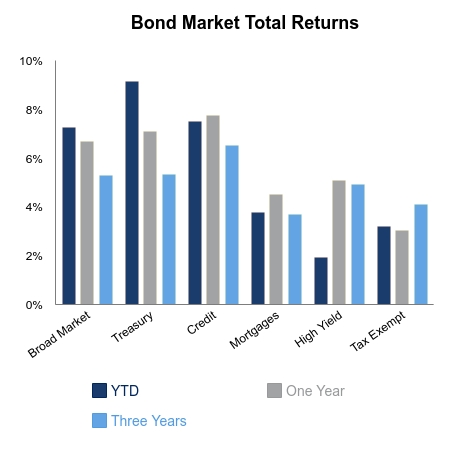

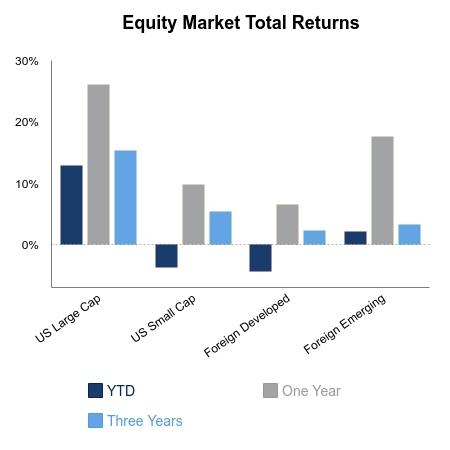

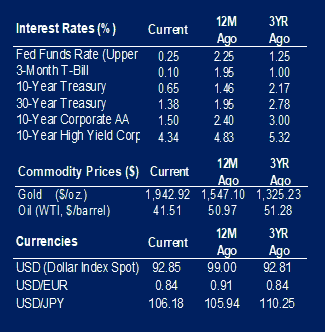

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.