Welcome to Five in Five, a monthly publication from the Investment Team at BTC Capital Management. Each month we share graphs around five topics that illustrate the current state of the markets, with brief commentary that can be absorbed in five minutes or less. We hope you find this high-level commentary to be beneficial and complementary to Weekly Insight and Investment Insight.

This month’s Five in Five covers the following topics:

- Fed Funds Wild Ride

- Stronger than Expected Employment Figures

- Declining Leading Indicators

- Growth Outperforming Value in 2023

- Equity Style and Sector Rotation Year-to-Date

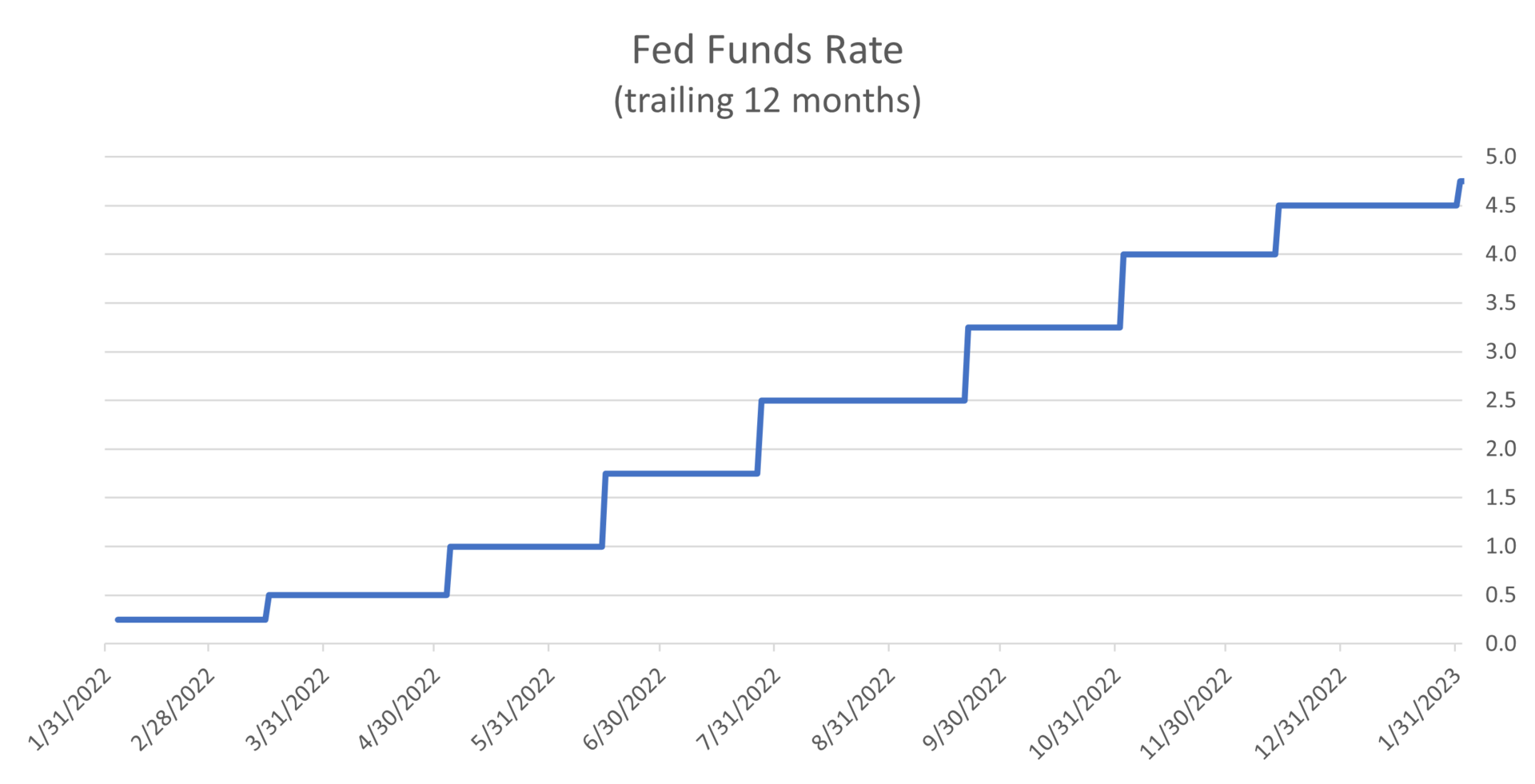

1. Fed Funds Wild Ride

- The Federal Reserve raised interest rates by 25 basis points at their last meeting.

- It was a downshift from their previous pace of 50 basis points per meeting.

- The Fed historically moves in a measured pace without random adjustments.

- When the Fed pauses, they are signaling no further interest rate increases are anticipated this cycle.

- In not wanting to reverse course, they may extend 25 basis point hikes beyond current market expectations.

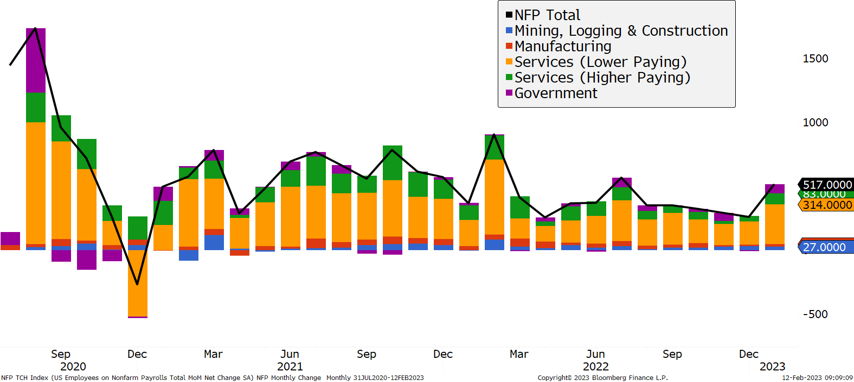

2. Stronger than Expected Employment Figures

- January Non-Farm Payrolls (NFP) showed the number of employees increased by 517,000 at those employers surveyed.

- This figure surprised economists who had projected NFP to continue to decline for the fifth straight month to 189,000.

- Similar one-month spikes happened last year in July and February.

- This rise indicated to markets that the economy remains strong, reducing the probability of the Federal Reserve cutting rates in 2023.

- Bond markets reacted to this stronger economic outlook with higher rates, the 10-year Treasury rose 20 basis points to 3.5% soon after the jobs announcement.

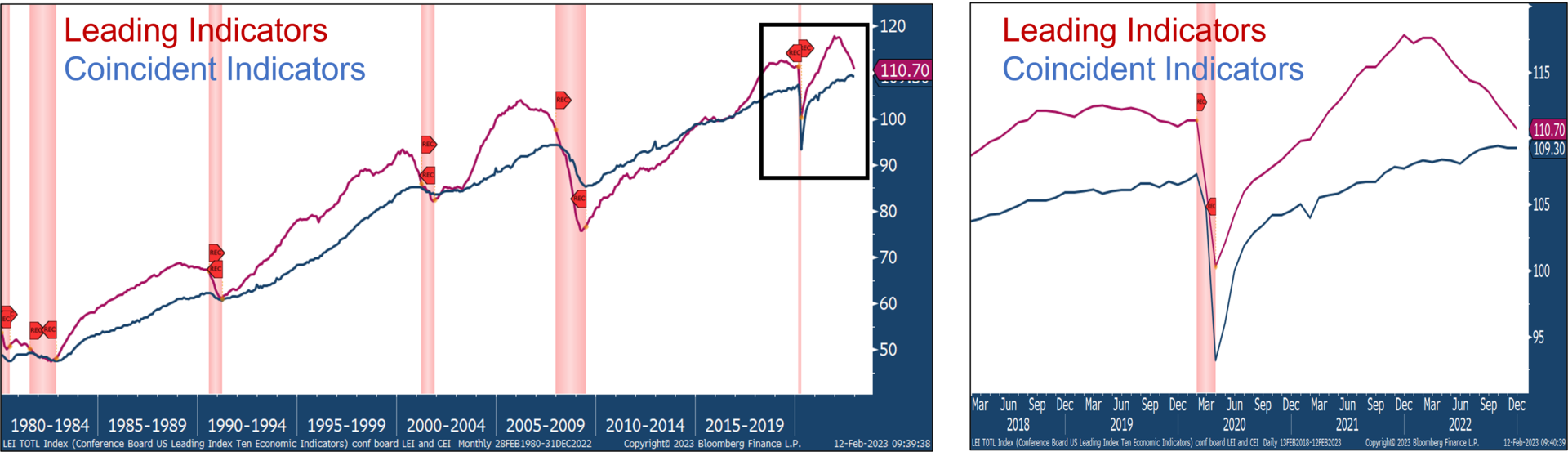

3. Declining Leading Indicators

- The above charts show the Conference Board’s US Leading Index of 10 economic indicators and Coincident Composite.

- These two indices will often cross when the economy is about to enter or is in a recession.

- After the recovery growth period following the pandemic leading indicators have been declining at a pace that would signal crossing the coincident indicators during 2023.

- The 12-month looking forward Cleveland Federal Reserve Fed Probability of Recession Forecast that uses the yield curve is at 63%. That measure has not been at this level without a recession dating back to 1959.

- ISM Manufacturing data continued to slide in January indicating manufacturing growth is negative.

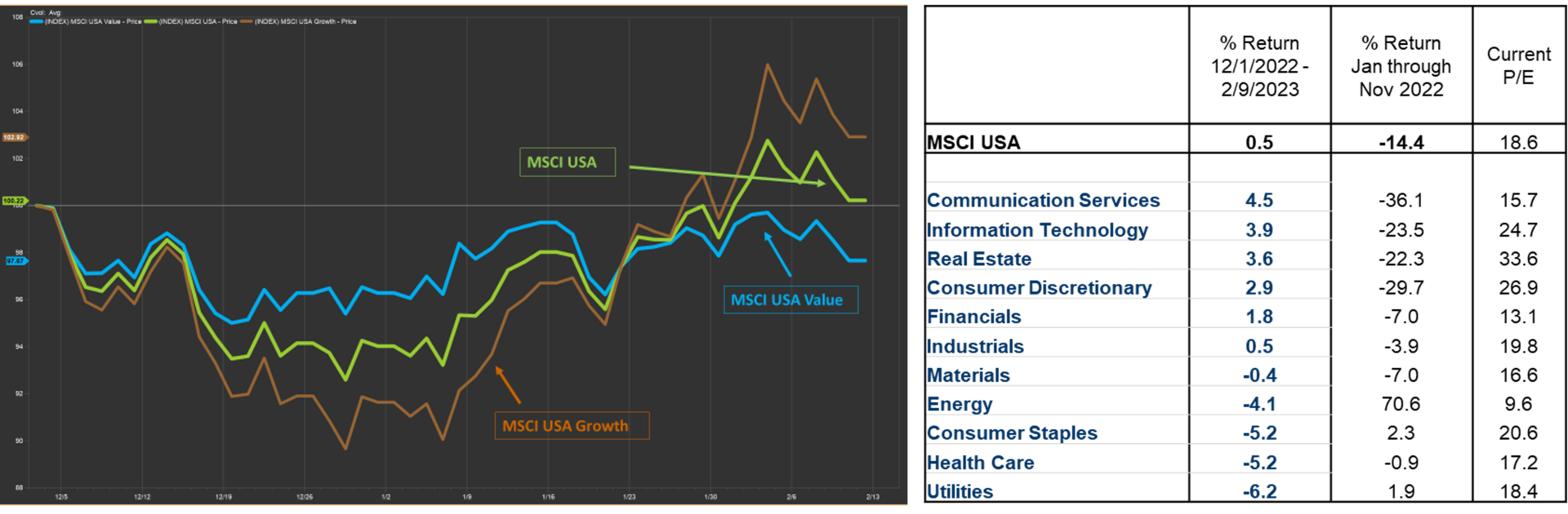

4. Growth Outperforming Value in 2023

- Since January of 2023, Growth has rallied and has outperformed Value and the overall broader market, a reversal of that experienced in 2022. Note the left-hand chart, which depicts the price movement of the MSCI USA Index, the MSCI USA Value Index and the MSCI USA Growth Index.

- Sectors that have rallied the most since December of 2022 were among the worst performing sectors for the first 11 months of 2022 (note the right-hand chart).

- Likewise, several sectors that have rallied the most since December of 2022 currently exhibit a higher price-to-earnings ratio (P/E) vs. other sectors (note the right-hand chart).

- It appears investors have rotated from Value orientated stocks into Growth stocks, whose relative P/E’s are higher, despite indications the Federal Reserve will continue to raise rates during 2023, which generally provide a headwind on valuations of Growth orientated stocks.

- With ongoing economic uncertainty and continuing downward earnings revisions, there is the potential that investors will “flight to quality” and rotate back into Value orientated stocks.

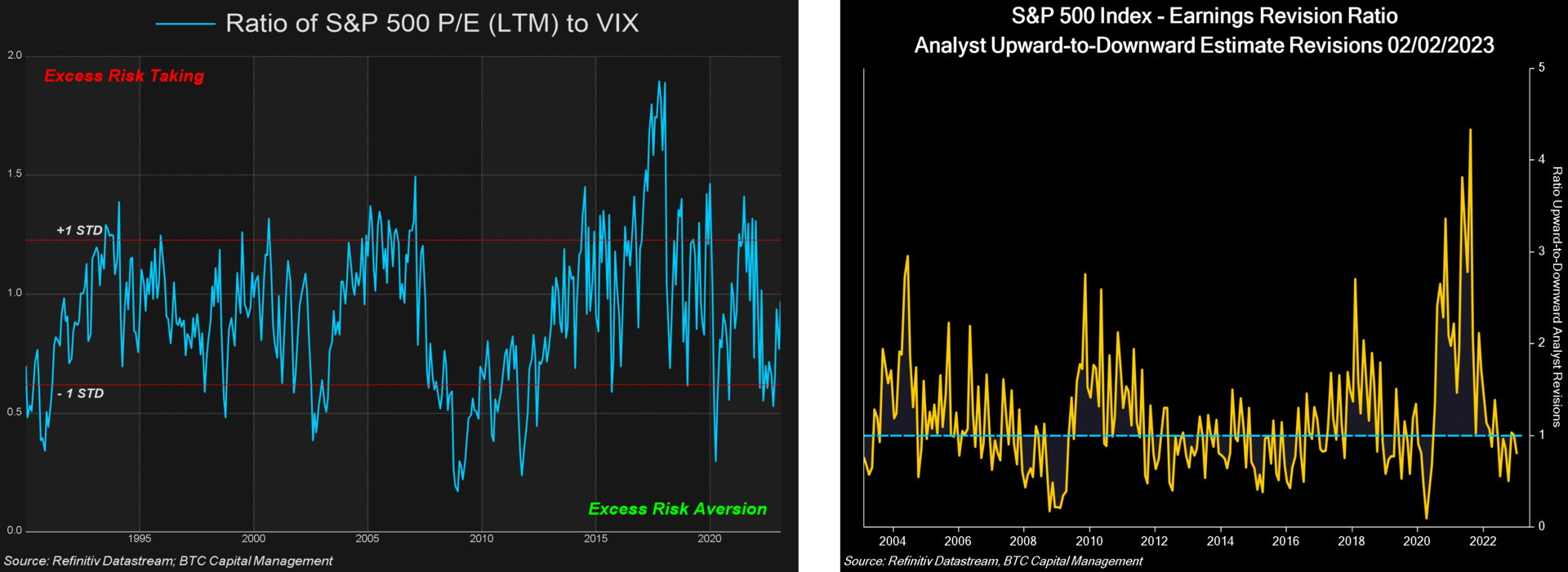

5. Equity Style and Sector Rotation Year-to-Date

- Surprisingly, given the apparent style and sector rotation, coupled with Fed policy, it does not appear as if investors’ risk-appetite is excessive. The chart on the left exhibits the ratio of the S&P 500 price-to-earnings (P/E) last twelve months (LTM) to the CBOE Volatility Index (VIX) as a measure of overall risk. Note this ratio lies within a bandwidth of +/- 1 standard deviation and is somewhat neutral regarding the riskiness currently assumed by investors.

- Currently the S&P 500 Index exhibits a price-to-earnings (P/E) ratio of 19.2x when considering its last twelve-month earnings (LTM) versus its average P/E LTM of 17.6x over the last 20 years.

- The CBOE Volatility Index (VIX) is a measure of 30-day expected volatility of the U.S. stock market. It currently stands at 21.0 modestly above its 20-year historical average of 19.3.

- We continue to monitor the trend in analyst earnings revisions, as this tends to indicate near-term market sentiment. Downward revisions continue to outpace upward revisions, although the near-term trend may be abating (note the right-hand chart). Overall, analysts continue to project year-over-year growth in earnings for calendar-year 2023, albeit 2.5% currently.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This document is intended for informational purposes only and is not an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.