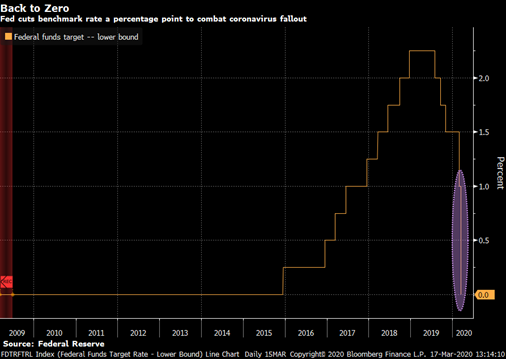

The Federal Reserve (Fed), along with six central banks from around the globe, launched the most dramatic monetary measures to boost America’s economy in its entire 105-year history. Pulling from its 2008 playbook the Fed has implemented plans at an aggressive pace to relieve key stress points in financial markets. Fed Chairman Jerome Powell recognizes he can’t singlehandedly offset the potential of an oncoming recession, although he’s still hoping to avoid a freezing up of financial markets that extends any prospective economic weakness. In an unprecedented Sunday conference call with reporters, Powell outlined the Fed would slash short-term interest rates to near zero and launch a fresh round of quantitative easing programs.

These actions were first and foremost focused on providing liquidity to financial markets, so they could continue to function smoothly. This action follows a week of high volatility in the treasury markets where yields swung by more than a full percentage point for a 30-year bond. The Fed’s playbook is very clear cut. First, stabilize treasury markets, the basis upon which other fixed income assets are priced. Second, pump liquidity (cash) into the financial markets so lending unfreezes, and borrowers can bridge the economic slowdown. Third, now that the Fed is all-in, it waits to see how fiscal policy fills in any gaps it cannot.

The tipoff play to reinvigorate the treasury markets was launched last week when the Fed offered $1.5 trillion in short-term lending to 24 of the country’s largest banks. These banks, known as primary dealers, function as the Fed’s exclusive counterparties when trading in financial markets. Primed with cheap money, these banks are now more willing to buy/sell inventories of treasury bonds and other securities. The Fed followed up by further announcing a $700 billion buyback plan (quantitative easing) of treasury and mortgage-backed securities. This has begun to entice buyers into the market and will clear a backlog of sellers, resulting in stabilization of prices.

The injection of liquidity will help high-quality bond issues trade more efficiently and encourage banks to extend credit to keep corporate liquidity problems from becoming solvency problems. This action has been followed by the central bank employing emergency powers under section 13.3 of the Federal Reserve Act to allow it to create the Exchange Stabilization Fund. This fund allows the Fed, with a guarantee of the Treasury, to lend directly to corporations.

The final call to action is for fiscal policy to be directed toward specific industries and broader consumption. Plans may include establishing sector-specific groups like the Air Transportation Stabilization Board, created in 2001 to divvy up economic stimulus packages offered by Congress. Once all these actions are in place it will still take time for markets to gain the confidence of investors and for consumers to turn the weak growth of the first half of 2020 into stronger growth in the second half.

Contributed by | Jeff Birdsley, CFA, Senior Managing Director, Fixed Income Manager

Jeff Birdsley is a Senior Managing Director for BTC Capital Management. Jeff has more than 25 years of investment experience. Jeff’s primary responsibilities include fixed income portfolio management and strategy. Prior to joining BTC Capital Management, Jeff was a fixed income portfolio manager for EMC Insurance Companies. He holds the Chartered Financial Analyst designation and is a member of the CFA Institute. Jeff earned a Bachelor’s degree in Finance from Iowa State University and a Masters of Business Administration degree from the University of Nebraska.

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.