We all know people who have been looking for a house over the last few months. This search story is similar across the country.

Lack of Supply + High Demand = Inflated Prices

Pre-2020, a common refrain was that millennials are just not buying houses. That they don’t want to live in the suburbs. That they want experiences instead. But things have changed since then. It may be the combination of being stuck in an apartment for many months and finally being able to afford a house. Not having to pay student loans and a lack of travel opportunities during the pandemic led to a stronger balance sheet for many millennials. They were ready to buy, and now all at once.

Supply

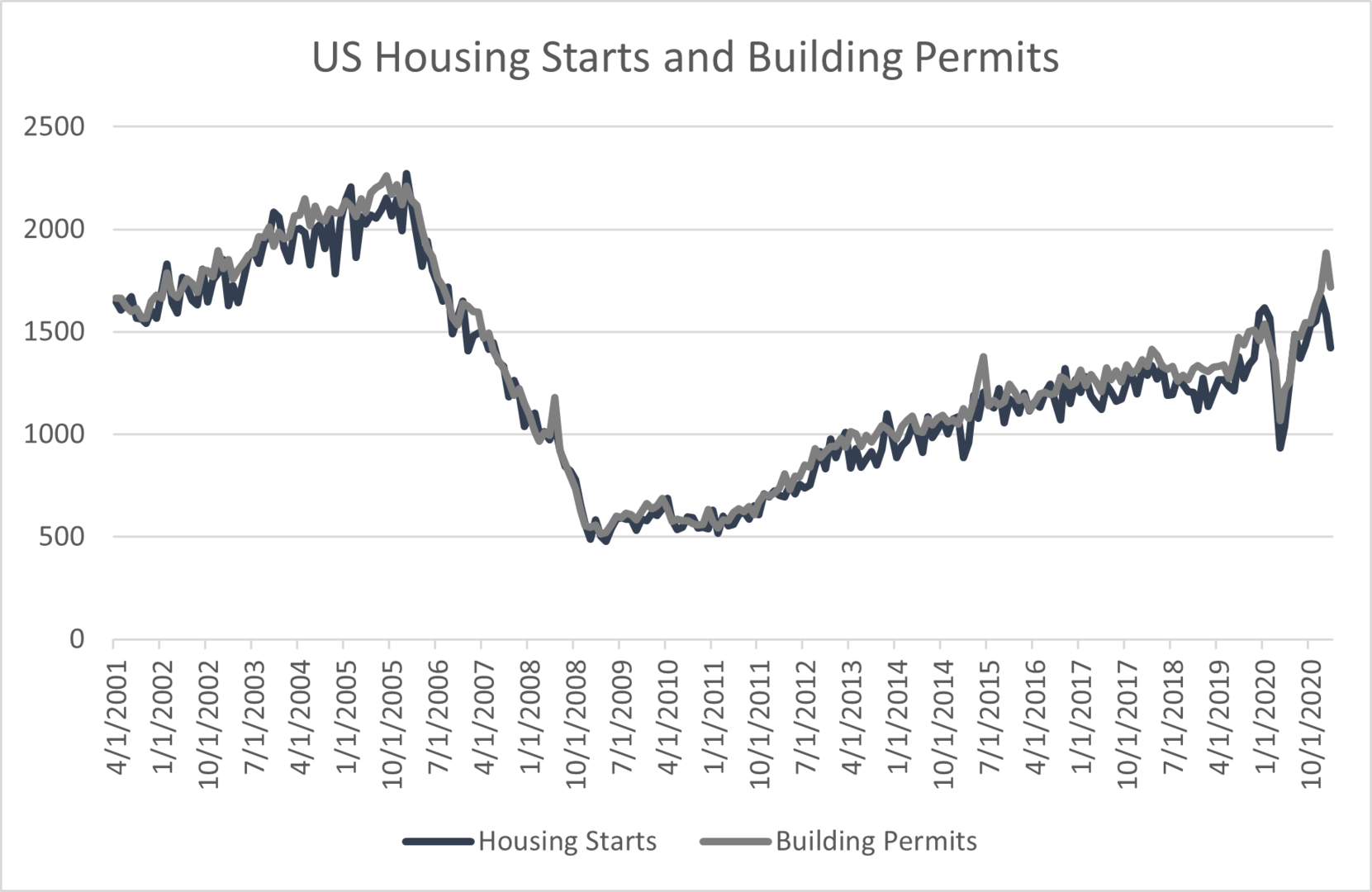

Builders were still licking their wounds after the financial crisis of 2008. There wasn’t much appetite to go out and build after so many had taken significant losses. Builders were operating to survive. They had been gradually building confidence that was made even more fragile by a lack of millennials interested in buying homes. Housing starts and building permit numbers were just getting back up to early 2000’s numbers as they approached their 2006 peak. Things started to pick up in 2019, more homes were being built and sold. Then there was a significant short-term pandemic-induced drop, as seen below. Now, activity has picked up significantly and developers cannot build homes fast enough.

According to the National Association of Realtors, as of December 2020, inventory levels were down to 1,070,000 active properties listed. This is a 16.4% drop from November 2020 and a 23% drop from December 2019.

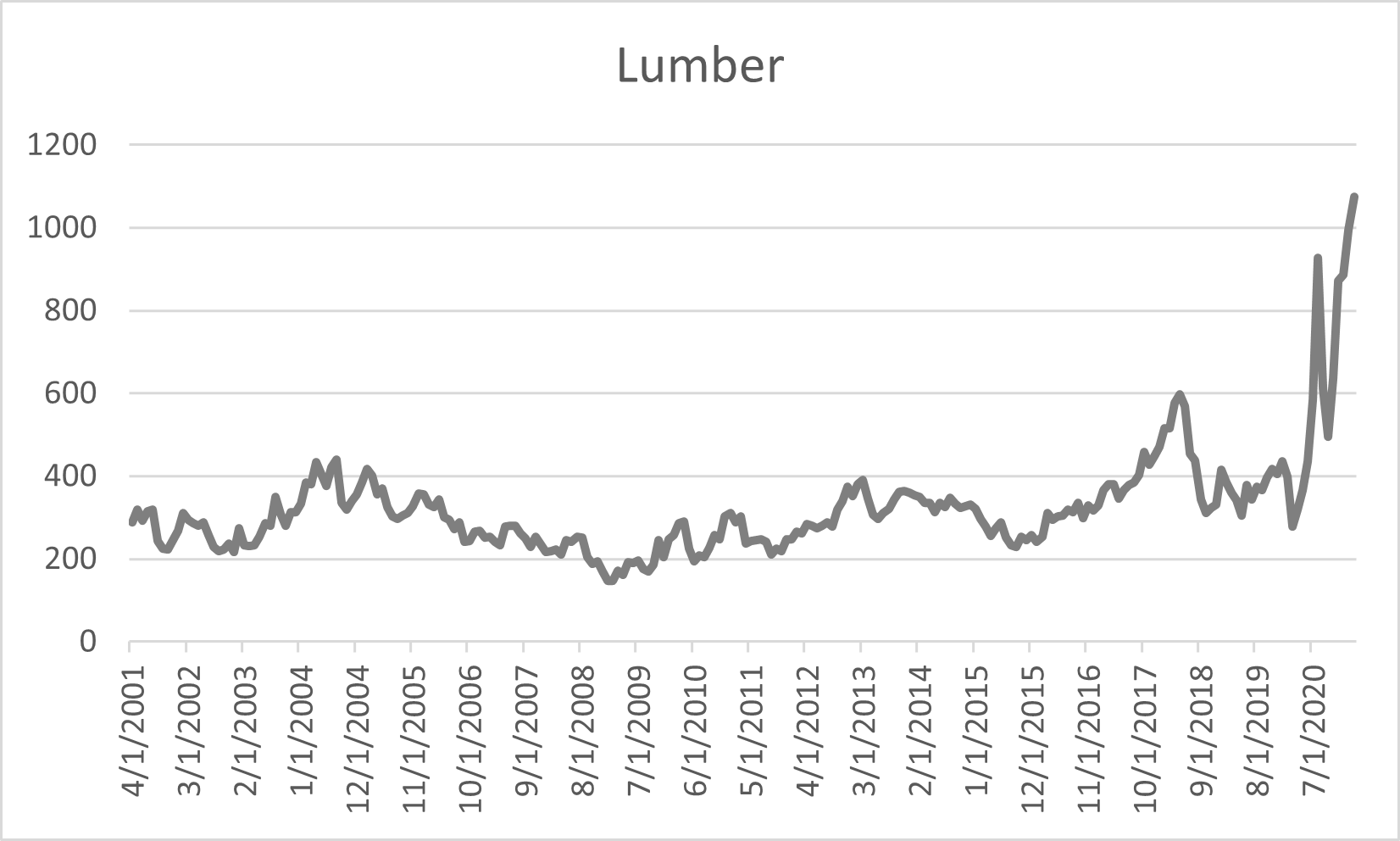

Another contributing factor to housing supply issues is the skyrocketing cost of building materials. COVID-19 restrictions, combined with trade tariffs on lumber from Canada, contributed to a remarkable increase in lumber prices. The Commerce Department reduced tariffs on Canadian lumber to 9% from 20% late last year. This has not led to a decrease in prices yet. The United States is competing with Asian and European markets for lumber. At the end of March, lumber futures crossed the $1,000 per thousand board feet level. The five-year average is $438. Some homebuilders are holding off on construction until prices decrease. Other homebuilders are passing on the price increases directly to buyers.

Demand

Demand for housing had been increasing in 2019. We saw this as both new and existing home sales picked up. The first two months of 2020 showed strength and then the pandemic took hold. People were scared they may lose their jobs. In April 2020, things started to stabilize. There were no experiences to be had and people were isolated inside. The housing rocket had launched, and low mortgage rates were the fuel. Housing sales then rose to levels not seen since 2006.

In February, existing and pending home sales growth was negative at -6.6% and -10.6%. You would think after the growth we have seen; the negative numbers mean a decline in demand. It doesn’t. However, it does show how tight the market it, there are just not enough homes.

Who is buying?

Leading the charge for home purchases are finally millennials. According to the National Association of Realtors, millennials were the largest generational group buying houses in 2020. People between the ages of 22 and 40 bought 37% of available homes. Gen Xers, those between the ages of 41 to 55 and the highest earners, were the second-highest purchasing generational group buying 24% of homes.

Another demand factor has been the availability of capital. Disposable personal income and the personal savings rate reached new highs in 2020. Reduced spending and stimulus payments were significant contributors. Individual investors and second home buyers accounted for 17% of home sales in February. A significant number of these purchases were cash sales.

Pricing

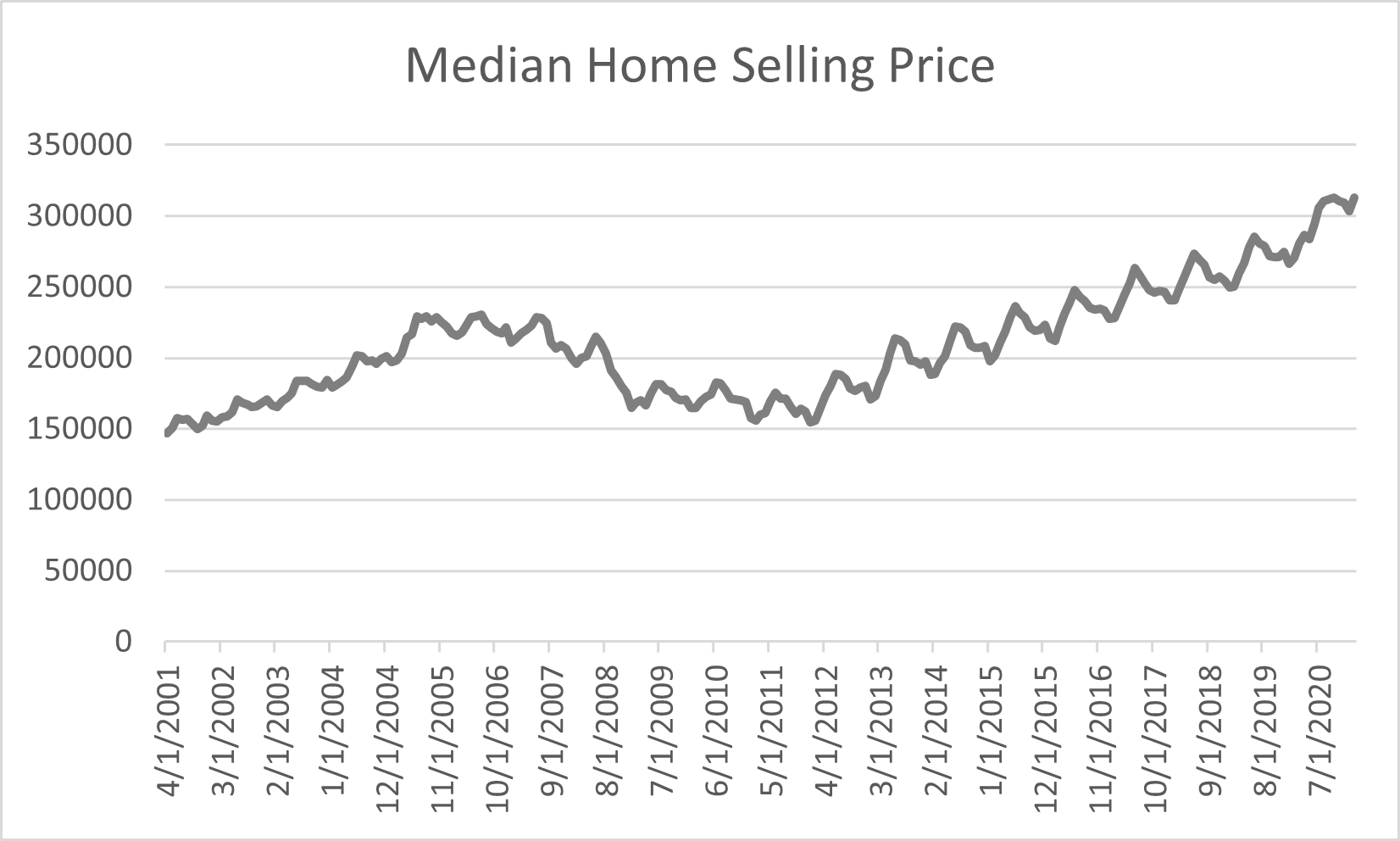

The combination of supply pressures and a surge in demand has contributed to home purchase prices accelerating. The median home selling price has gone from $270,400 in February 2020 to $313,000 in February 2021. That is a 16% increase over one year. Significantly more than inflation. The increases are not concentrated to geographic areas. All U.S. regions have seen increases in prices.

Home price increases will be more evenly distributed around the United States going forward. Remote work has contributed to employees in high-cost-of-living areas to migrate to more affordable regions. People will chase affordability creating some evenness in prices across national metropolitan areas.

This is Not a Bubble

It is unlikely we are going to see a sharp turnaround in the short run. The factors contributing to the price increases are a lot less artificial than those of the financial crisis of 2008. The expectation is for prices to flatten as more homes hit the market. Builders have started putting more homes in development. Supply will chase demand. Cost of materials will be passed on to buyers.

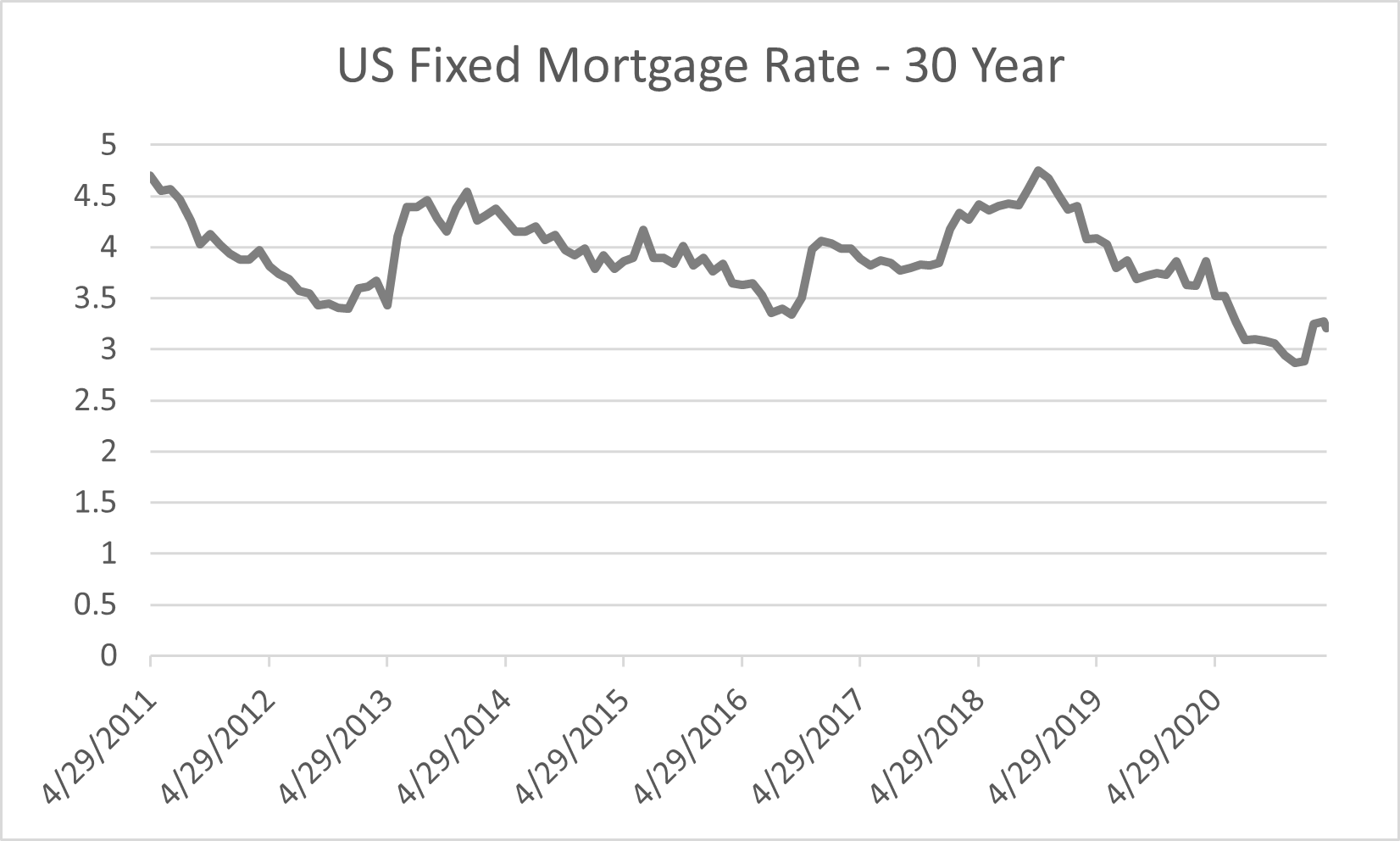

Mortgage rates have started picking up after the U.S. 30-year fixed mortgage hit a low of 2.85% in February. Rates were at 3.27% at the end of the first quarter. It is likely a bottom that materialized in February. Increasing rates will likely contribute to a pullback in demand.

This market is fundamentally different from the pre-financial crisis market. We do not expect a significant drop in housing prices. Instead, the expectation is for a plateauing of prices as supply issues are addressed and interest rates rise. Prices will stabilize as the relationship between supply and demand gets closer to equilibrium.

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.