The S&P 500 was down slightly on the week as sector dispersion was again a major factor. Materials were up more than 4% while both energy and financials gained. The NASDAQ was down 3.3% as technology bellwethers were sold aggressively following good earnings. The NYSE FANG+ Index was down 5.0% on the week. The previously strong semiconductor space was down 4.2% and has underperformed the S&P 500 by roughly 10% over the last month. This all occurred with Treasury yields falling, which is normally met with technology outperformance. The Bloomberg Barclays Aggregate Bond Index was up 0.4% on the week and has rallied 1.3% from its March low.

Economic data was strong for the week, although the surprise factor is no longer present. GDP for the first quarter gained 6.4%. The report showed strength in consumer spending with personal consumption expenditures up 10.7%. Investment and exports weighed negatively on the report. The Employment Cost Index rose 0.9% in the first quarter, its highest quarterly gain since 2007. The year-over-year number remains low following a drop in 2020, but two consecutive quarterly gains could really catch some attention should this transpire in the July release.

Personal income set a record with a 21.1% gain in March. It is the third monthly number of more than 10% in the last 12 months, and this level had previously never been achieved going back to the 1946 series inception. It is probably not surprising the cryptocurrency total market capitalization has gone up 10x in the past year.

Construction spending came in well below expectations as did the ISM Manufacturing report. The April ISM came in at 60.7 versus 64.7 the previous month. Bond yields fell on the day as growth momentum appeared to slow, despite still being high. This is an environment when bond yields normally fall not increase, despite lagging Consumer Price Index readings that are high. The question is whether growth will stay up in the 4-6% range for several quarters or if we are getting one-time pull forward in demand.

ADP private payrolls missed consensus as well with an April reading of 742,000 job gains. The current consensus is for 925,000 private payroll gains on Friday when the Bureau of Labor Statistics reports its monthly jobs report. It appears the potential is there for this report to have outsized ramifications to the growth and inflation narrative over the coming weeks.

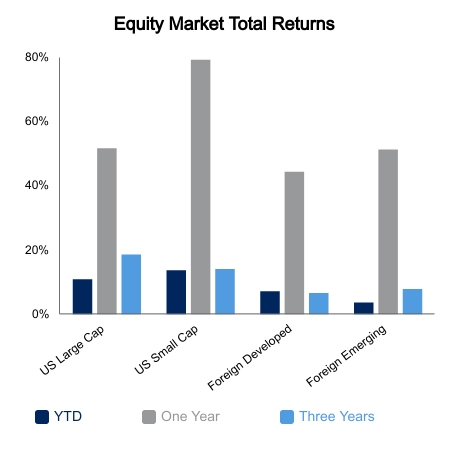

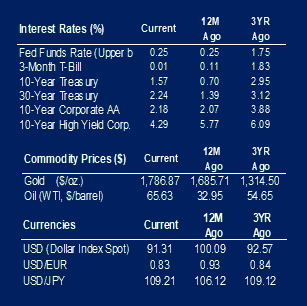

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.