How to Measure the Market

Indexes have been a quick and relatively easy way for investors to track broad market performance since Charles Dow developed the Dow Jones Industrial Average (DIJA) in 1884. The index, which tracked 11 railroad stocks, was the first broadly used indicator of U.S. equity market performance. The number of companies represented by the index increased to 30 in 1928 to give a broader representation of the market. The limited amount of data available in 1884 led to a unique index construction methodology. The price of a holding was used as the weighting mechanism. Weighting mechanisms determine the impact of a single company on the index. If a company was trading at $100 with a market value of $1,000,000, it would have a higher weighting than a company trading at $10 with a market value of $10,000,000. This price-weighting and limited scope decreased the value of using the DJIA as a broad market indicator. In 1926, Standard Statistics Company, later Standard & Poor’s (S&P), developed a 90-stock index computed daily. Company weights in the index were determined by the market value of a company’s outstanding shares compared to the price-weighted approach taken by the DJIA. In 1957, the number of stocks in the S&P index was expanded to 500. The S&P 500 was a more accurate reflection of the combined performance of U.S. public companies. It was a broad, well-diversified index. Since the advent of the market-weighted index, we have seen a wide variety of additional providers and indexes. For large cap equities the index we prefer at BTC Capital Management is the MSCI USA Index. This index holds over 600 companies and shows broad representation of the market. There are a few more index weighting methodologies we will not cover in this piece.

The Introduction of the Index Fund

Investment management evolved into the development of the first publicly traded index fund, or exchange-traded fund (ETF), created by John Bogle in 1975. This was a cheap way to get passive exposure to the broad market. There has been incredible growth in fund flows to ETFs. You put your money in a well-diversified passive fund and forget about it. However, more recently, there have been concerns on how “well-diversified” index funds really are.

Index Concentration

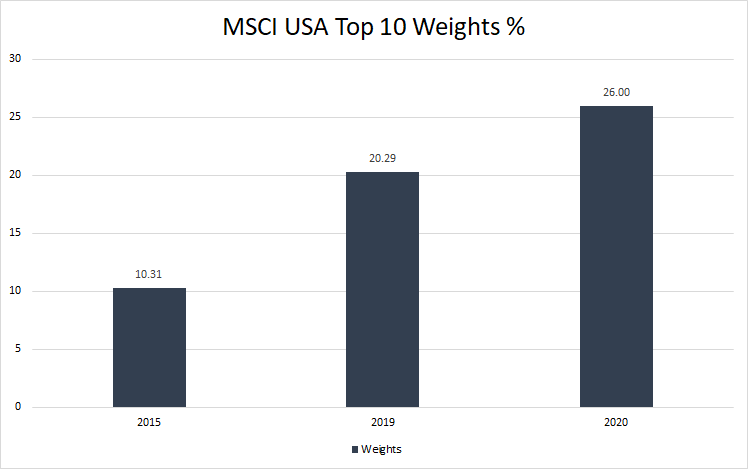

We have seen increasing concentration of index fund company weighting in two handfuls of large stocks. Just five years ago, the top 10 companies of the MSCI USA Index made up 10% of the index. Last year, the weight of the top 10 doubled to 20%. As of Sept. 30, the top 10 companies make up 26% of the index. That is an increase of close to 30% in just a year.

This increasing concentration is leading to a less-diversified index. Correlations between securities are increasing with most of the weighting coming from three sectors: Information Technology, Communication Services and Consumer Discretionary. This de-diversification of the index fund has major consequences for investors looking for broad market exposure.

Why is this a concern?

Concentration of portfolios leads to increased risk exposure. Portfolios using these indexes are not only exposed to systematic risks, that face the entire market like global pandemics, they are also exposed to idiosyncratic risks. These are the risks faced by individual companies and may even be extended to sectors. As mentioned earlier, the top 10 companies of the MSCI USA currently make up 26% of the benchmark. Sector concentration is also high, with the Information Technology sector making up close to 30% of the benchmark.

Throwing money in a passive fund is no longer the well-diversified bet that it has been historically. The concentration in individual securities and in a few sectors could lead to index contagion. This is a handful of companies experience a downturn leading to the entire index losing a significant chunk of its value We see a growing number of investors using index funds as their primary investment strategy. A drop in the highest weighted companies can fundamentally impact long term investment goals.

Active Management

Our active management approach does not seek to chase returns. We are risk managers and we build portfolios that seek to maximize return relative to risk. We pay close attention to portfolio structure and we seek to balance our exposures. We analyze the impact to the portfolio of adding more risk. We see active management as not just about selecting high-flying companies, but an exploration to achieve proper balance. We ask ourselves questions like, what are we sacrificing for more risk? How much risk can we afford in a particular portfolio? What exposure weights negatively impact the risk profile of a portfolio?

Passive index funds do not consider these questions. There is no oversight to prevent concentration. There are no managers balancing risk and working to increase diversification. Passive funds are great for people who want broad exposure to the market along with the increased risks of concentration. However, active management provides a risk aware portfolio construction.

Source – Benchmarks and Investment Management – Laurence B. Siegel The Ford Foundation

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.