The 2021 second quarter earnings season has started out strong. So far, 20% of S&P 500 companies have reported and earnings and sales growth are coming in a lot stronger than expected. Earnings have grown over 100% from the second quarter of 2020. The growth has been led by the Financials sector as they benefit from releases of loan loss reserves. The Energy sector was also a significant contributor to earnings growth as oil companies recover from the decimation in earnings from last year. The growth is 18% better than expected. Sales are up 19%, which is 4% better than expected. Growth here is led by the Consumer Discretionary sector as demand picks up in 2021. Double digit earnings growth is expected through the end of the year.

Retail sales were up 0.6% in June from May. The increase comes as a surprise especially since a decline of 0.40% was expected. The growth shows strong and increasing demand in services. Growth was led by increases in electronics and appliance stores and miscellaneous store retailers. There was a dip in motor vehicles and parts dealers as limited supply negatively impacted sales.

OPEC reached a deal with the UAE which allows them to increase oil production. The cartel has been in the difficult position of balancing production limits which keeps prices elevated with partners wanting to produce more to generate more revenue. There has been a jump in demand for the commodity as worldwide activity picks up following last year’s lockdowns.

Housing is moving in a positive direction as housing supply expectations are improving. Construction on 1.643 million houses was started in June, while the expectation was for 1.59 million. The higher-than-expected number is 6.3% better than last month. Companies are building again as pricing for commodities like lumber dips.

Businesses stocked up on inventories in May. Business inventories were up 0.50%. An increase usually signals businesses expect increases in demand which is a bullish signal. The expectation was for growth of 0.35%. Last month, inventories were up 0.10%.

Consumer sentiment as measured by the Michigan Sentiment Indicator dropped in July. The drop to 80.8 was attributed to inflation and Delta variant concerns.

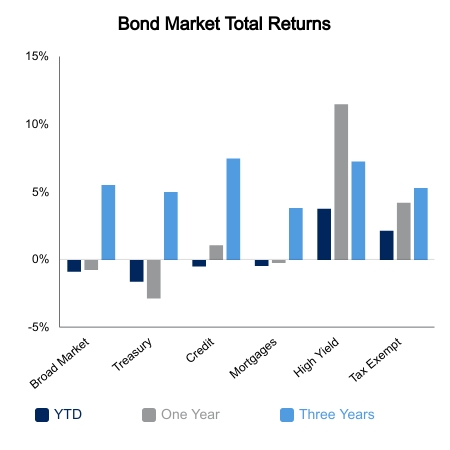

|

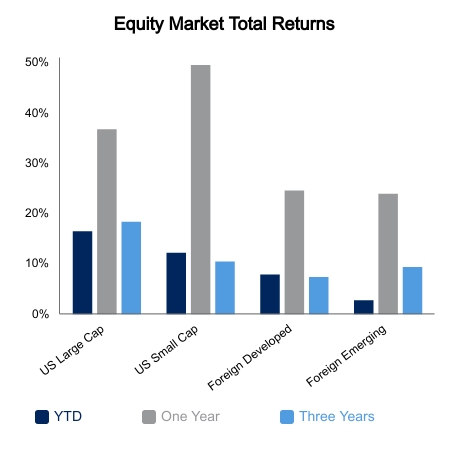

|

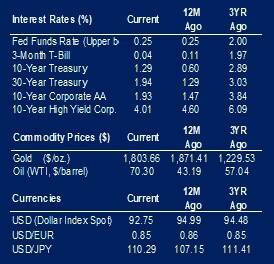

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.