Small Caps Surge in Wild Week for Equity Markets

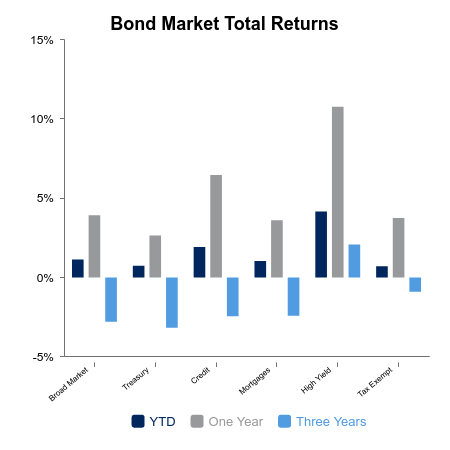

Small caps began moving higher after a better-than-expected CPI report. Changing presidential polls added more fuel and pushed them up 9.2% on the week. The S&P 500 was down 0.8% as the crowded technology trade began to unwind. The NASDAQ finished down 3.5% on the week. Core bonds were up 0.9% as September rate cut probabilities moved to 100%.

Small caps rallied 11.5% over a five-day stretch. It was the largest five-day gain since the COVID lows in early 2020. It was also the largest five-day gain that occurred outside a major bear market low in at least 30 years. Making things interesting was the fact that technology shares, especially large cap, sold off sharply. It was well known that long tech, short small caps was a crowded trade. It would unwind in a violent manner. The Russell 2000 outpaced the S&P 500 by 10% over a five-day period. This was the highest dispersion since 1987 and the second-largest ever.

Semiconductors had a daily drop of 6.8% following comments from both presidential candidates and the continued rotation in the markets. It was the largest daily decline since March 2020. Meanwhile, homebuilders were up 16.6% in the largest ever five-day rally outside of a bear market low.

Falling Inflation Positions the Fed to Cut

The key economic data point this week was CPI, which came in lower-than-expected last Thursday. The core reading was up 0.1% versus the previous month. The headline number was negative 0.1%, which spooked more than a few economists and analysts. There continues to be a wide divide in views on whether a recession is quickly approaching versus a soft-landing and reaccelerating economy. The negative CPI print is a red flag for those that fall in the former camp.

The Leading Economic Index came in at -0.2% versus the previous month. It continues to improve but has now gone 28 consecutive months without a positive monthly reading. This is the longest stretch without a positive reading in the entire 65-year series.

The market moved September to a 100% probability of a cut following the CPI report. The 10-year Treasury traded down 4.15%, its lowest level since March. The other key development is the Treasury curve beginning to steepen, although it remains inverted in most cases. Fed rhetoric supported the notion of beginning to cut interest rates with improving inflation readings, although they seemed to indicate July was unlikely to see action.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.