There was a significant drop in personal income in February; it decreased by 7.1% over the month. This is after January saw an increase of 10.1%. The main contributing factor to the decrease was that there were no stimulus checks sent out in February. The January increase was greatly impacted by stimulus payments; therefore, this drop is coming from a high. The March personal income number should also reflect the impact of stimulus payments received that month.

Personal consumption expenditure (PCE) for February was down 1% after a strong January at 3.4%. This decrease is influenced by the reduction in the personal income number. The decrease was led by spending on pharmaceutical products and recreational items. Higher oil prices partially offset the decrease in addition to increases in services. The personal savings rate was also impacted by the decrease in personal income. The recording of 13.6% comes after a strong January number of 20.5%, a record high.

The number of pending home sales were down 10.6% in February. This drop is not indicative of a weakening housing market, it shows the opposite. Lack of supply is contributing to a tight housing market leading to increased housing prices. The S&P/Case-Shiller Home Pricing Index shows a 11.1% increase in home pricing in the 20 metropolitan areas covered over the last year. Over the month, home prices are up 1.2%.

Consumer confidence continued its march up. The March reading of 109.7 shows an optimistic consumer. The expectation was for a reading of 96. Last month, it was at 90.4. This month’s reading is the highest reading since February 2020. The Michigan Sentiment Indicator was also higher than the expected 83.6, at 84.9. Last month’s number came in at 83.

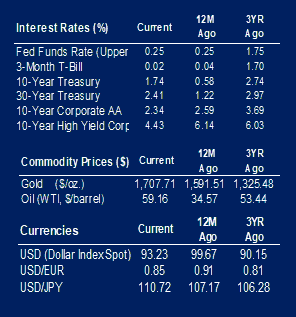

Oil pricing was down close to 3% this week. The commodity closed the first quarter up 21.69%. This positive performance comes after a significant 2020 price decline. The increase has been attributed to increasing demand for the commodity and OPEC supply cuts.

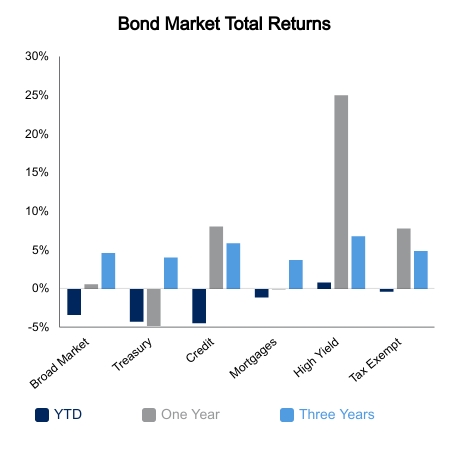

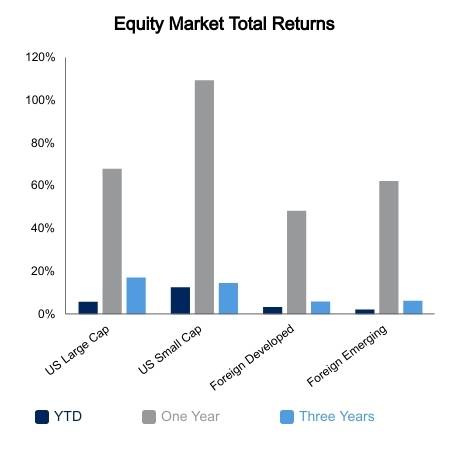

Equity markets closed March up 4.38%. This contributed to a first quarter return of 6.17%. All sectors were up for the month led by utilities, industrials, and consumer staples.

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.