Second quarter GDP revisions show slower growth than was expected. The revision shows GDP growth of 2%. This is down from the initial reading of 2.1%. The downward revision is due to lower than expected local government spending, exports, private inventory investment, and residential investment. Strong personal consumption expenditure (PCE) was the major positive contributor to the growth.

We continued to see PCE growth in the third quarter. The revised PCE growth for July was 0.60%. This tops the 0.50% initially reported. Purchases of recreational goods and vehicles led the growth in PCE. This could be indicative of optimistic and confident consumers using their dollars to purchase things they want, assuming their needs have been met. Consumer spending makes up roughly 68% of the U.S. GDP.

Personal income growth on the other hand was revised down to 0.10% from 0.30%. The number is lower, but we are still seeing growth. The increase was attributed to rising compensation and government social benefits.

Consumer sentiment as measured by the University of Michigan dipped in August. The reading of 89.8, down from the previous month’s 92.1, was lower than the expected 92.4.

Purchasing manager numbers are pushing the bottom threshold of optimism. Traditionally, PMI numbers of over 50 have been seen as a sign of strength in manufacturing. The 50.4 reading for August, although better than the expected 49, shows signs of weakness in manufacturing. The ISM manufacturing number broke through the bottom threshold with an August reading of 49.1. This is lower than the expected 51.5.

Wholesale inventories grew by 0.20% in July. This index surveys merchant wholesalers for their inventory numbers.

Pending home sales contracted by 2.5% in July. Sales growth was expected to stay flat at 0.35%. This comes after July’s strong growth of 2.8%. The July construction spending number was revised downward to 0.10 from 0.30. Despite the downward revision, growth was still better than the previous month’s contraction of 0.72%.

Equity markets rallied this week. The S&P 500 was up 1.7% from last week Wednesday’s close. This increase has been attributed to positive reaction to the announcement of trade talks between the United States and China. Crude oil prices stayed flat this week with growth of 0.1%.

|

|

Contributed by | Kuuku Saah, CFA, Investment Analyst

Kuuku is an Investment Analyst with seven years experience in the Wealth Management division of Bankers Trust, most recently on the Trading Desk as a Securities/Trading Specialist. Kuuku’s primary responsibilities include supporting our portfolio managers in security and portfolio analysis. Kuuku attended Drake University and double-majored in finance and economics. During that time he interned with BTC Capital Management.

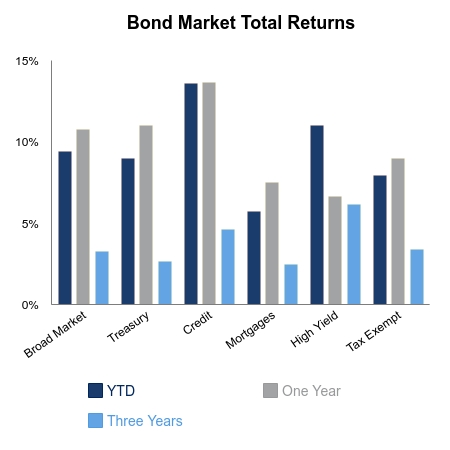

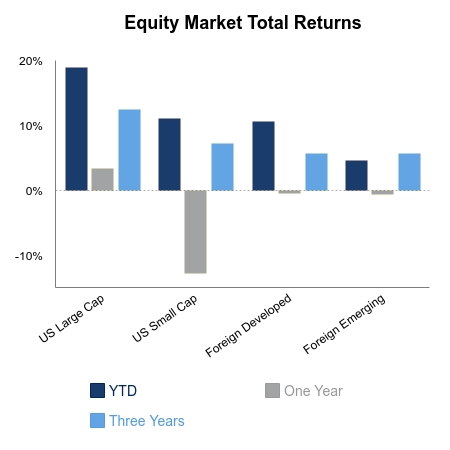

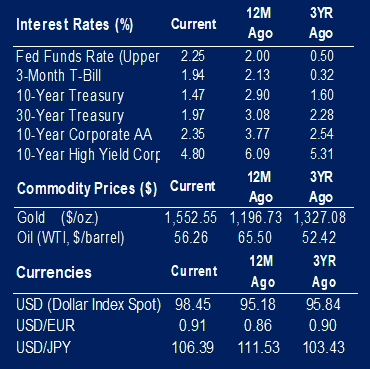

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.