Financial markets experienced significant turbulence over the past week

Key Takeaways

- Stock market volatility continues to surge.

- The price of oil remains elevated.

- The Fed remains steadfast.

Stock market volatility continues to surge

Investors have experienced a continued increase in volatility since the U.S. – Iran conflict began. Recall our Weekly Insight from February 25 in which we characterized what appeared to be a “sustained near-term uptrend” in the VIX Index, a measure of 30-day implied volatility for the S&P 500 Index compiled by the Chicago Board of Options Exchange (CBOE). As of February 27, the VIX stood at 19.9, an increase of approximately 33% over its close as of December 31, 2025. The VIX has surged by almost 23% from the end of February through April 1. Not the April Fools’ joke investors want to experience.

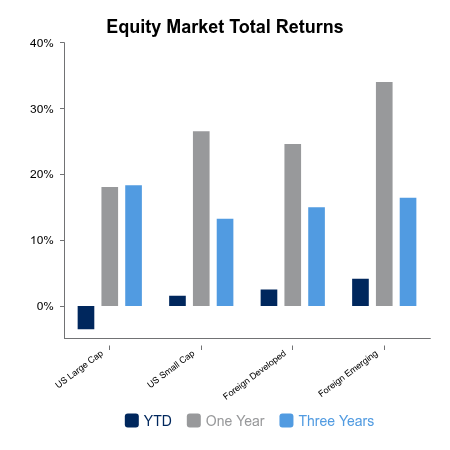

Over the past week, equity markets have experienced both bad and good. While the Russell 3000 Index declined 0.2% for the week, the MSCI All‑Country World Index ex-USA posted a positive return of 1.0%. This hides a decline from March 25 through March 30, when concerns about the conflict depressed market sentiment and each index declined by 3.8% and 2.7%, respectively. Subsequent comments from the Trump Administration coupled with statements from the President of Iran to end the conflict abated near-term concerns after which each index climbed 3.7% and 3.8%, respectively, through April 1.

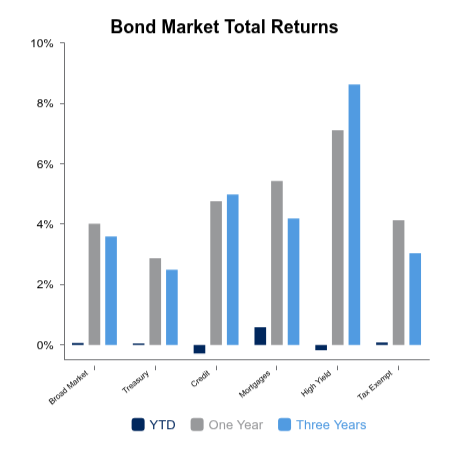

Investment‑grade bonds rose 0.2% for the week.

The price of oil remains elevated

Volatility may also be observed in the oil markets, and additionally distillates such as gas. Brent crude rose by 16% over the past week. For the month, Brent crude rose 59% in March, its steepest monthly rise, which exceeded the increases experienced during the 1990 Gulf War. Intuitively, gas prices have also risen. According to AAA, the national average price per gallon of regular fuel rose from $2.98 as of February 26 to $4.08 currently, a 37% increase in pump pricing.

The Fed remains steadfast

As of March 30, Fed chair Powell reiterated a “wait and see” policy, stating “There’s sort of downside risk to the labor market, which suggests keep rates low, but there’s upside risk to inflation, which suggests maybe don’t keep rates low. You’ve got tension between the two objectives.” Surprisingly, the Conference Board reported a rise in consumer confidence in March to 91.8 from February’s 91.0, driven by an increase in consumers’ assessment of current business and labor market conditions.

|

|

Sources: BTC Capital Management, FactSet Research Systems, Inc., FTSE Russell (an LSEG Company), MSCI Inc., American Automobile Association (AAA), The Conference Board

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.