Volatility increases in the face of near-term macro events

Key Takeaways

- Surge in equity volatility

- Equity markets de-risk

- Macro uncertainty heightens

Surge in equity volatility

Over the last week, volatility has increased given the geo-political situation between the U.S. and Iran. The Chicago Board Options Exchange Volatility Index (VIX) rose to levels last seen in April. Week-over-week the VIX rose from a recent low of 15.4, as of June 4, to 22.2 as of end-of-day June 10, an increase of 44%. Recall the VIX is a measure of market expectations of near-term volatility conveyed by S&P 500 Index option prices.

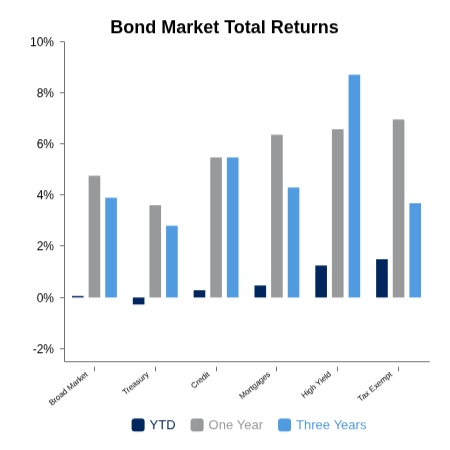

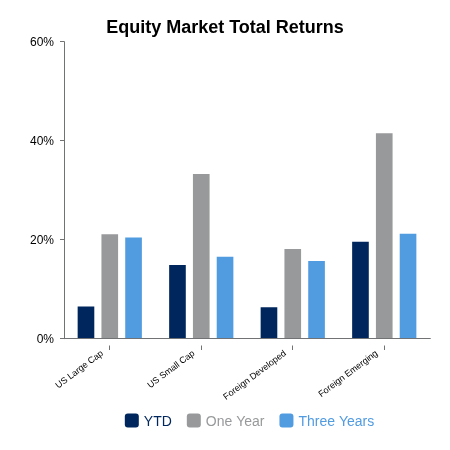

For the week, the Russell 3000, a broad measure of U.S. publicly traded companies, declined 3.6%. Outside the U.S., the MSCI All-Country World Index ex-USA, a broad measure of foreign developed and emerging markets, declined 3.7%. Bonds declined 0.2%.

Equity markets de-risk

Year-to-date (YTD), equity investors have experienced solid returns, albeit via a choppy path. Given the recent volatility coupled with the macro-events YTD, investor sentiment has been dynamically driven by near-term phenomena. Valuation continues to be a question many investors weigh, or at times disregard when considering forward performance based on recent market observations. As interest rates rose within the U.S. last Friday in response to the unemployment report, investors globally exited technology-related companies due to their perception of valuation as they applied it to these companies. The MSCI All‑Country World Information Technology Sector Index fell 9.6% over this past week. While this index has risen 35.1% YTD, driven primarily by earnings growth attributed to its underlying constituents enhanced by animal spirits motivated by a “fear of missing out,” the recent drawdown exhibits an uncertainty that continues to influence investors.

Marco uncertainty heightens

On the economics front, the Bureau of Labor Statistics (BLS) released its unemployment report for May. BLS reported nonfarm payrolls increased by 172,000, materially exceeding consensus expectations of 100,000. BLS reported the unemployment rate stayed at 4.3%, similar to April’s report. Job gains were reported in leisure and hospitality, local government, and health care. This drove an uptick in yields, as the yield of the U.S. 10-year Treasury rose above 4.5%, its highest since mid-May.

The National Federation of Independent Business (NFIB) released its Optimism Index for May, which fell to 95.3, continuing its trend below its 52-year average of 98.0. The NFIB also reported its Uncertainty index rose to 91, remaining materially above its historical average of 68.

Thanks to Maggie Richards for her contribution to this Insight.

|

|

Sources: BTC Capital Management, FactSet Research Systems, Inc., LSEG I/B/E/S, FTSE Russell (an LSEG Company), MSCI Inc., S&P Global Inc., Bureau of Labor Statistics, National Federation of Independent Business

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.