Inflation continues to run hot. The Consumer Price Index (CPI) for March was released this week. The increase of 8.5% over the year and 1.2% from February to March shows a continuation of price increases. A lot of this increase can be attributed to sharp rises in energy. Fuel oil was up 22.3% and gasoline, up 18.1% over the month, contributed to an increase of 11.0% in the energy segment of the report. From last year, fuel oil and gasoline were up 70.1% and 48.0%, respectively. Prices for used cars were the only major decline in the month, down 3.8%. CPI excluding food and energy was up 6.5%. The high inflation number increases the likelihood of more aggressive Federal Reserve action. The probability has increased for a 0.50% raise at the Federal Open Market Committee May meeting.

Declining Consumer Buying Power

Despite a strong increase in hourly earnings in March, the data point was unable to keep up with the increase in prices. Year-over-year, hourly earnings grew by 5.6% in March. Month-over-month, it is up 0.4%. Real hourly earnings, after adjusting for inflation, are down 2.7% from March 2021. Consumers may be taking on more debt to offset the decline in their buying power. Consumer credit increased significantly in February. The credit increase to $41.8 billion is a jump from the prior month’s $8.9 billion and higher than the expected $17.5 billion.

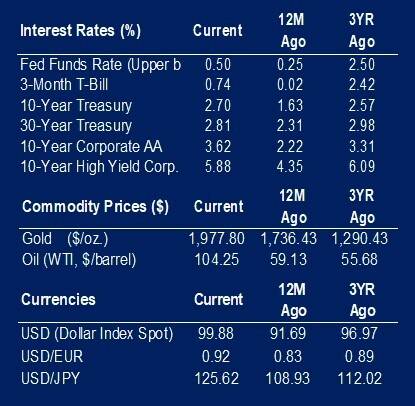

30-year Mortgage Rates

- 30-year mortgage rates broke 5% this week.

- The average 30-year mortgage has stayed under 5% since 2011.

- The increases reflect the rising costs of capital.

Earnings Season

We are at the very beginning of earnings season. Only 7% of S&P 500 companies have reported. Earnings are coming in a little better than expected with initial growth of 6.3%. This is 9.5% better than expected. Sales are growing 1.9% better than expected at 10.9%. The faster pace of sales compared to earnings indicates the potential for narrowing margins as costs increase. However, it is still early, and the pace may change as more reports come through.

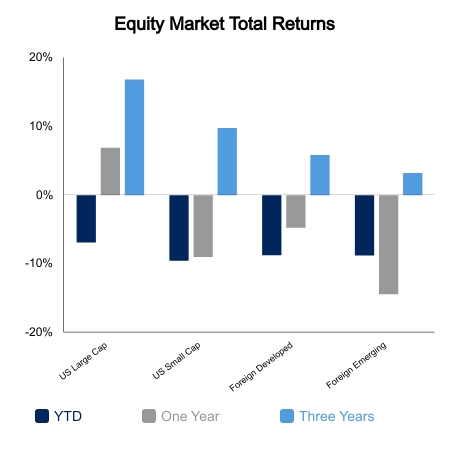

Equity Markets

Equity markets are down this week and the S&P 500 lost 0.73%. The losses were led by information technology, down 2.57% and communication services, down 2.51%. The energy sector continues to be a strong performer, up 4.08% this week.

|

|

Source: BTC Capital Management, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.