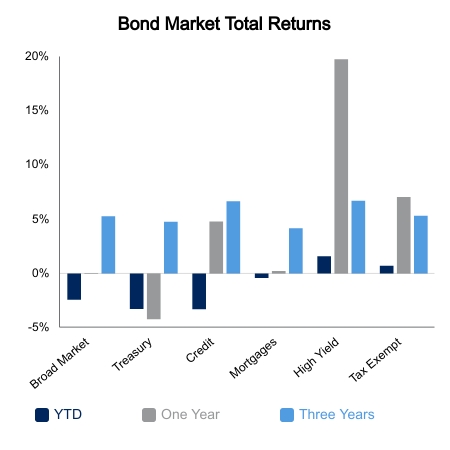

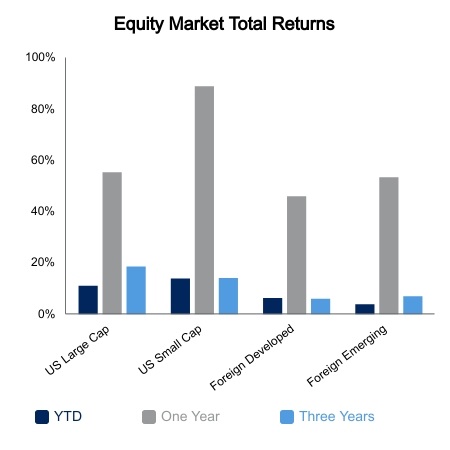

The S&P 500 pushed higher despite some softness mid-week. Upside was achieved by the more defensive sectors as growth and small caps struggled to gain traction. The S&P 500 ended the week up 1.2%, but small cap stocks finished in the red. Small caps have been weak of late as have many of last year’s big winners. Capital continues to flow into the more well-established large cap names. The Bloomberg Barclays Aggregate Bond Index posted its second consecutive weekly gain. Interest rates on longer bonds have pushed lower amid global virus-related issues.

Economic data was robust for the week. Regional manufacturing prints were again near their all-time highs as the New York and Philadelphia region reported this week. Retail sales came in well ahead of expectations for March with a 9.8% monthly gain. Housing starts beat expectations and were up 37% versus the prior year. Yearly comparisons are going to be skewed in March and April, but this series is up 44% from two years ago and at its highest level since 2006.

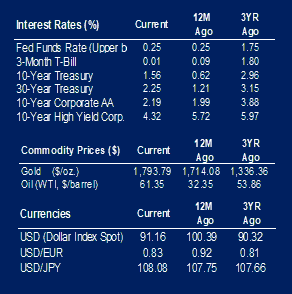

Consumer sentiment as measured by the University of Michigan survey came in a bit softer, especially on the future expectations side. This is worth monitoring as a big gap between current conditions and future expectations often indicates the Treasury curve will flatten. Also of note was the one-year inflation expectation rising to its highest level since 2012. The Federal Reserve (Fed) is watching inflation expectations and here we have evidence of it increasing noticeably. We have the Bank of Canada and the Bank of Japan reducing accommodation at the margin. It could indicate the Fed may be following the bond markets’ lead in the timing of future rate hikes and act sooner than their current stance suggests.

About 20% of S&P 500 companies have reported first quarter earnings. The numbers thus far are robust with earnings up 55% and sales up 6%. Earnings surprises and sales surprises are also very strong as is forward guidance. Despite this, single stock reaction has been rather muted to results, as much of it was anticipated.

Next week there is a Federal Open Market Committee meeting. It is unlikely the Fed will deviate from its path regarding inflation expectations, but it only takes the slightest of hesitation for the market to sniff it out and make some ripples. GDP for the first quarter will also be released and the consensus is currently at 6.0%.

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.