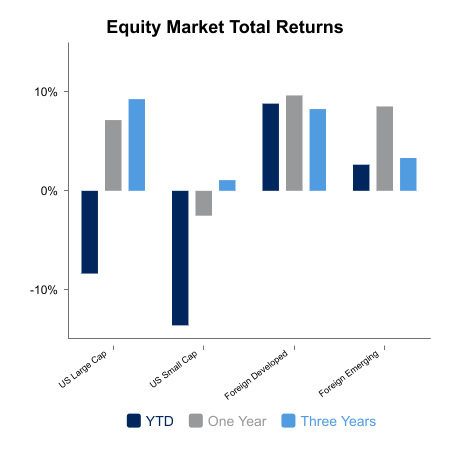

Equites Bounce on the Potential for Lower Tariffs

Equities bounced back on the week amid ever changing comments from the White House regarding tariffs. There was some modest give back in the rhetoric over how tough the U.S. will be regarding China, but nothing has officially changed. Comments that appear to lean toward better outcomes are often contradicted later in the day. In the end, the quick drop in markets left it vulnerable to rallies on less bad news and this has played out. The S&P 500 is up 1.9% on the week. The more oversold indices jumped more with the NASDAQ up 2.5% and small caps up 3.0%.

Economic data remains okay but has yet to reflect tariff policies. Some forward indications of capex and trucking activity are showing weakness.

- Jobless claims remain low at 222,000.

- New home sales came in better than expected.

- Renaissance Macro Research noted that current capex intentions have only been lower in 2008-2009 and during COVID. This is over a 23-year period.

- Trucking volumes have dipped notably this year and post tariff announcements.

- Knight Swift, the largest full truckload carrier, reported earnings this week and noted that customers importing from China have taken a wait-and-see approach with some cancellations.

The Trump Put

Fixed income has benefitted from the slight improvement in tariff rhetoric. It is speculated that rising yields are the primary Achilles heel to the White House tariff plan. Softer tones become more pronounced as yields rise, which is an indication of a Trump put, although we remain far from a complete walk back in the policies. It remains to be seen if a rising stock market and lower bond yields emboldens a tougher tone on tariffs and we get caught in this circle of focusing too much on markets as it oscillates within a range.

30-year Treasurys peaked over 5.0% post tariffs, but now reside at 4.77%. 10-year yields are well off their year-do-date highs and sit at 4.31%. Corporate bond spreads have made a decent move lower and should continue to do well if equities don’t make new year-to-date lows.

The Fed appears to be taking a wait-and-see approach, as well. This caused some strong remarks from President Trump regarding firing Jerome Powell. The bond market did not take too kindly to the idea of losing central bank independence and sold off along with the U.S. Dollar Index. Once again, the market moves got the attention of the White House and the tone softened thereby leading to lower bond yields and stabilization in the U.S. dollar.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.