There was a significant contraction in GDP in the first quarter of 2020. Initial numbers show a contraction of 4.8%. We have not seen such a sharp drop since the financial crisis. The deceleration was led by weak consumer spending. The number could have been worse had it not been for an increase in government spending. A larger contraction is expected in the second quarter.

Manufacturing continues to be weak. The Markit PMI manufacturing number for April came in at 36.9, which is lower than the expected 38.3. Purchasing managers’ confidence has been significantly impacted by the virus. The Markit service number was lower than the already low expectation. The service number for the month was 27 compared to the expected 32.5. The PMI is a diffusion index. Numbers lower than 50 are indicative of a contraction.

Durable goods orders for March were down by 14.4%. Orders for transportation equipment led the decrease. The industry saw new orders decline by 41%. Excluding transportation, new orders were down 0.2%.

Consumer confidence dipped to 86.9 in April from the previous month’s 118.8. This number is in line with the consensus estimate of 85. This number could dip even more as the unemployment rate increases. Initial unemployment claims for the week ending on April 18 was 4.427 million. Total claims are expected to increase as nationwide shutdowns continue.

The S&P 500 is up 5% over the last week. This comes amid indications that local economies may be opening after lockdown closures. Fears of a “second wave” or resurgence of the virus remain. The last week takes month-to-date performance for the index up to 13.86% and narrows the year-to-date loss to -8.45%.

We are in the midst of 2020 first quarter earnings season. Earnings growth for the quarter is not comparable to previous quarters due to the pandemic and impacts on global economies. With 31% of companies reporting, earnings contracted by 19.4% from last year’s first quarter. Year-over-year sales growth remains positive at 1.6%. We expect companies to feel the full brunt of the pandemic in the second quarter. Current estimates have earnings contracting by 30% and sales down by 9%. The best performing sectors this season have been companies in defensive sectors like consumer staples, utilities and healthcare.

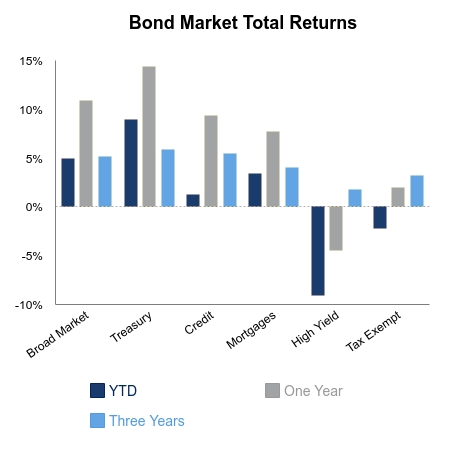

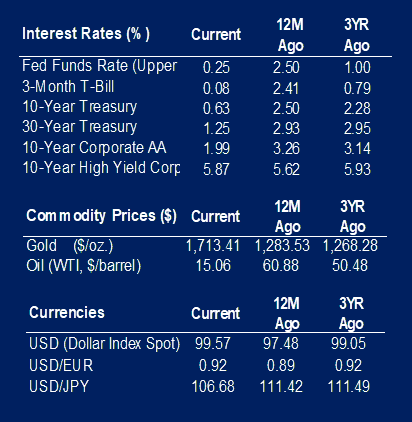

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.