Relief Rally and Longer-Term Uncertainty

Key Takeaways

- Relief Rally cuts March losses for global markets.

- Federal Reserve stuck between conflicting mandates.

- ISM Services PMI data shows firms shifting toward cost controls.

Global equity markets experienced a significant relief rally, driven by optimism regarding a fragile two-week ceasefire in the Gulf region. As of yesterday’s close, U.S. equities climbed 3.2% for the week, while international markets advanced 5.2%. This rally followed a difficult close to March, which saw domestic markets undergo four consecutive weeks of declines, falling 5.0% and marking the worst monthly return since early 2025. The pause in hostilities led to a sharp decrease in energy prices as West Texas Intermediate oil fell from $112.95 to close at $94.41 following the ceasefire announcement, relieving inflationary pressures.

While lower oil prices initially brought bond yields down, investor behavior transitioned to a “wait-and-see” approach. The market remained constrained by uncertainty regarding forthcoming inflation data and hawkish sentiment derived from recent Federal Reserve minutes. Consequently, the U.S. 10-year Treasury yield fluctuated, rising to 4.34% during the week, before closing at 4.29%. A similar holding pattern was observed in the inflation-sensitive 1-year Treasury, which settled at 3.68%, showing negligible change for the week.

Minutes from the Federal Reserve’s March meeting, released this week, revealed a policy committee stuck between conflicting mandates, as the energy shock affects both growth and inflation. The uncertainty surrounding the magnitude and duration of the oil shock is not clear yet, and Fed officials have historically been inclined to look through temporary price shocks and pause on further rate changes as they wait for further data.

What data Fed officials saw this week was data characterized by a resilient but slowing U.S. economy, where robust headline hiring contrasts with mounting inflationary pressures and emerging signs of weakness within the service sector. March nonfarm payrolls recorded a net gain of 178,000 jobs, representing a significant rebound from February’s revised loss of 133,000 jobs and surpassing market expectations. While the unemployment rate fell slightly to 4.3%, this decrease was attributed to a contraction in the labor force rather than the overwhelming demand for new hires.

In contrast, ISM Services PMI data pointed to waning momentum in the service sectors, which accounts for around 70% of U.S. economic activity. The headline Services PMI declined to 54.0 in March from 56.1 prior. While remaining in expansionary territory (above 50), the deceleration reflects mounting uncertainty among firms regarding persistent price increases and a shift toward cost control. The ISM prices paid index surged to 70.7 in March, the highest reading since 2022, while employment contracted to 45.2 from 51.8 prior reflecting a shifting trend for future hiring.

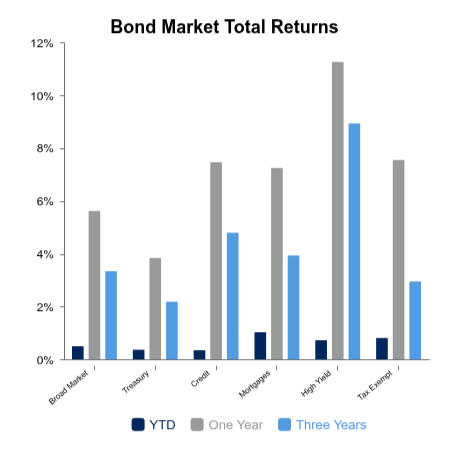

|

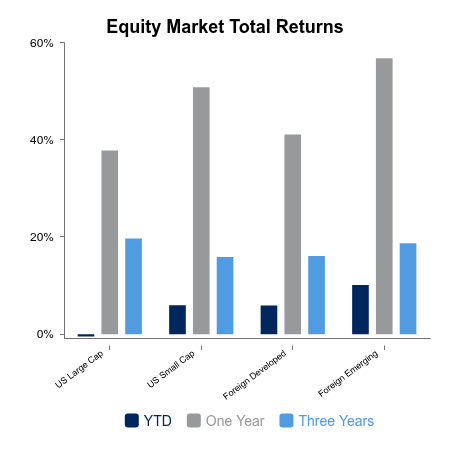

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.