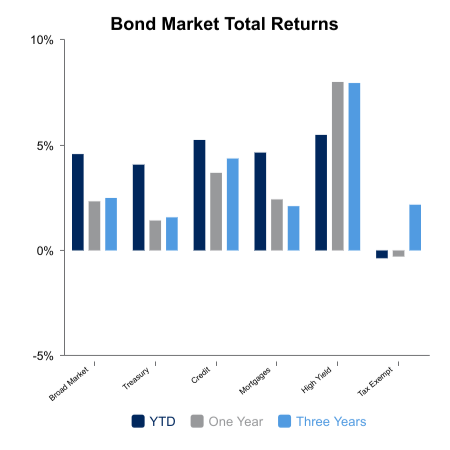

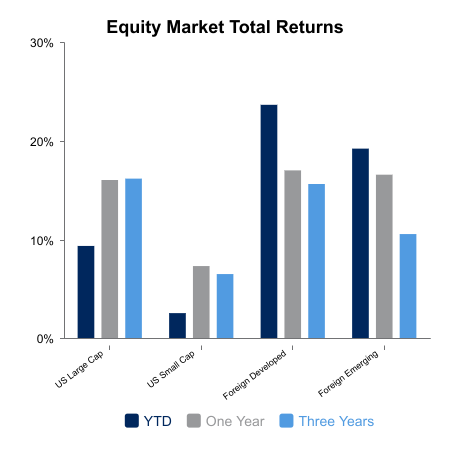

Equity markets fell during the week as investors took profits from record high levels. The S&P 500 Index fell 1.1%, while the Nasdaq Composite dropped 2.5%. The Magnificent 7 lost 2.8%. Small caps declined 2.5% for the week. Bond indices fell 0.3% during the week.

Strong Retail Sales Despite Lingering Inflation

A key inflation metric, as measured by the Core Producer Price Index (which excludes food and energy prices), came in higher than expected. It rose 0.9% versus the prior month, the largest monthly increase in three years. Economists note that with this latest result, inflation is still a potential threat to the economy.

Despite lingering high prices, retail sales for July came in strong, rising 0.5% from the prior month, spurred by demand for motor vehicles. June’s retail sales were also revised higher. Consumers have continued to remain resilient by bolstering economic activity, despite a softening labor market and lingering relatively higher rates of inflation.

Housing starts for July came in higher than expected, led by strong growth in multi-family construction units, which reached a two-year high. Homebuilders have remained cautious as higher input costs and relatively higher mortgage rates have dampened demand and increased the supply of available inventory.

Solid Results for Second Quarter Earnings

Second quarter earnings season is wrapping up and results have come in generally higher than expected. Year-over-year earnings growth for the second quarter is expected to be 12.9%, higher than forecasts from earlier this year. Approximately 80% of companies have reported higher than expected earnings. The Communications Services and Technology sectors have led the way with regards to earnings growth. Third quarter earnings growth is currently forecasted at 8.2%. Calendar year 2025 earnings growth is currently forecasted at 10.2%, which has increased recently.

Foreign Markets Outpace U.S.

Foreign equity markets, both developed and emerging, have outpaced U.S. equity markets thus far, year-to-date. However, earnings forecasts for MSCI EAFE have been decreasing recently as analysts have revised their forecasts downward.

Mega Cap Stocks: “Priced to Perfection”

Despite the strong earnings results, there remains much uncertainty regarding how the rest of the year will play out. Valuations are at already lofty levels, with the S&P 500 Next Twelve Months price-to-earnings (NTM P/E) currently at ~22.5X, at the very high end of its long-term historic range. While investors have generally adopted a “risk-on” mentality, many long duration stocks are “priced to perfection” as expectations for growth are high. The market has penalized those companies who may have met current earnings forecasts but have reduced earnings guidance for the remainder of the year.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.