Markets traded up 2.7% after last week’s trade off. Some of the pop may be attributed to the strength in earnings reports for retail companies this week. Retail is not dead yet, and it looks like traditional retail companies are gearing up for a marathon. Most of the growth in retail sales came from e-commerce, which is expected. However, surprisingly, we are also seeing growth in traditional retail. Larger retail companies are adjusting their businesses for the evolving retail landscape. Companies are heavily investing in providing solutions that meet their customers where they are. Does the customer want things delivered? They’ll deliver. Does the customer want to pick-up? They’ll pull it off the shelf and have it waiting. Does the customer want to walk around the store for a bit? They’ll have friendly salespeople available. The transition to this model has been expensive. Yet, successful retail companies are finally seeing returns from these investments. It also helps that consumers are confident; unemployment is low and wages are rising.

Retailers are closing out another positive earnings season. With 95% of S&P 500 companies reporting, earnings for the second quarter have grown by 3.1%, which was 5.6% better than expected. Revenue grew even more than earnings at 4.7%, which was 1.3% better than expected. Analysts are still signaling a contraction in the third quarter, but we are expecting growth in the fourth quarter and for the entire year.

This week has also seen revisions in earlier reported economic numbers. Most of these revisions reinforce earlier views. Retail sales were revised to 0.7%, beating the expected and previous month’s growth of 0.3%. The revised productivity number of 2.3% continues to show economic strength when compared to the expected number of 1.2%.

The new numbers for the week also pertain to manufacturing. The Empire State Index, a New York State manufacturing survey, and the Philadelphia Federal Index, a survey of manufacturing conditions in the Federal Reserve’s Third District, both show increasing confidence in manufacturing. The Empire State number was at 4.8 and the Philly Fed’s number was at 16.8. This compares with the expected 1.1 and 10 respectively.

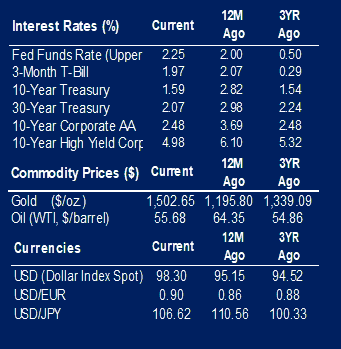

The spread between the 10-year and 2-year Treasury continued to decrease this week. The spread turned negative for the second time this week on Wednesday.

|

|

Contributed by | Kuuku Saah, CFA, Investment Analyst

Kuuku is an Investment Analyst with seven years experience in the Wealth Management division of Bankers Trust, most recently on the Trading Desk as a Securities/Trading Specialist. Kuuku’s primary responsibilities include supporting our portfolio managers in security and portfolio analysis. Kuuku attended Drake University and double-majored in finance and economics. During that time he interned with BTC Capital Management.

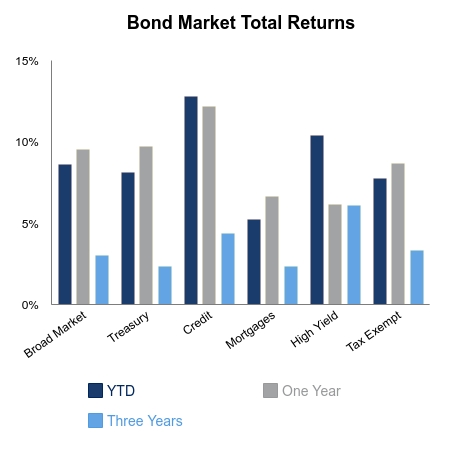

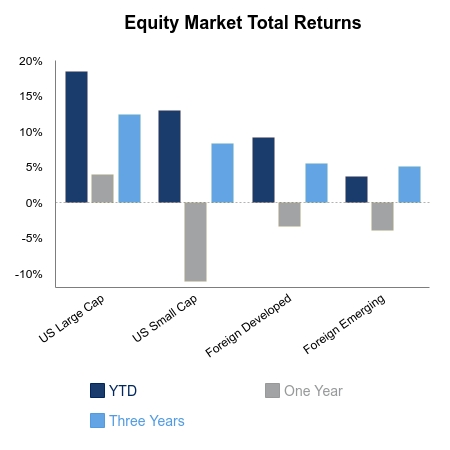

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.