Bear Market Rally or New Bull Market?

Equities sold off this week, marking an end to an eight-week run that saw the S&P 500 advance 17%. The S&P 500 was down 3.1% on the week, while the NASDAQ fell 3.9%. With short-term overbought conditions resolved, the market will find out if it has the legs to begin a new bull market advance. The S&P 500 now sits 13% lower on the year, which isn’t all that extreme. However, the duration of the decline is becoming noticeable. The 200-day moving average for the S&P 500 has been falling for 86 consecutive days. This is the third longest stretch in the last 30 years.

Changing Outlook for Bonds

The 10-year Treasury yield has reversed sharply higher this month, rising more than 50 basis points (bps) off its July low. Quite a lot has changed that could impact the direction of yields over coming months.

- The market is now pricing in 127 bps in hikes by December versus the previous 94 bps

- The market is now pricing in 141 bps in hikes remaining this cycle versus the previous 94 bps

- The implied Federal Funds Rate for December 2023 is now 70 bps higher versus July

- The $280 Billion Dollar Chips Act was signed into law on Aug. 9

- An even larger Inflation Reduction Act was signed into law on Aug. 16

- This week student loan forgiveness was announced and could amount to $300 billion

The Fed has continued to signal a higher for longer outlook on the Federal Funds Rate and the market obliged with some repricing this month. What is more relevant for yields, especially longer-dated maturities, are the government spending programs amid already high inflation readings. A big risk for long bonds is prioritizing government spending over stable prices. Actions taken this month appear to shed important light on the matter.

Can Equities Rally Amid a Weakening Economy?

Economic data remains weak with some shockingly so. Housing is at the front of the economic weakness. New homes sales are down 38% over the last six months. This was only lower once during the recession of 1980 for the dataset beginning in 1963. Jobless claims have leveled off and for now suggest it may be harder for economic data to continue to surprise to the downside. Markets will be geared up for Fed Chair Jerome Powell’s talk at Jackson Hole tomorrow. Consensus is that he talks tough on inflation and attempts to slap back some of the recent equity run. But should stock prices break higher, many funds will be offsides and the chase may see another run of strong gains.

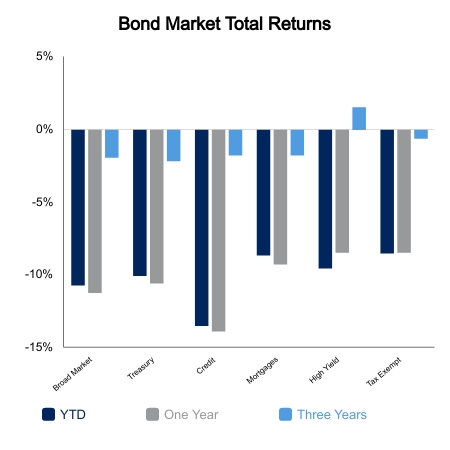

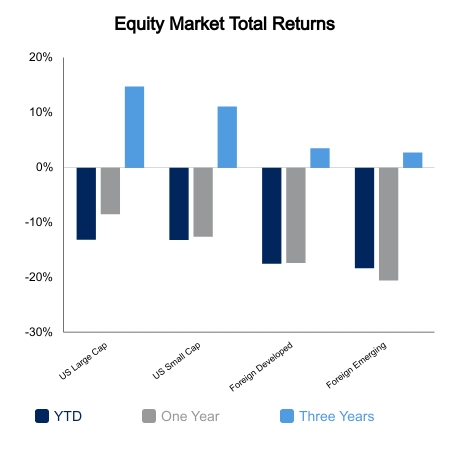

|

|

Source: BTC Capital Management, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.