Preliminary U.S. GDP numbers for the second quarter were released this week. U.S GDP declined by 32.9%. This officially puts the United States in a recession if you go by the 1974 rule of thumb definition established by former Bureau of Labor Commissioner, Julius Shiskin. He defined a recession as two consecutive quarters of negative GDP growth. I think, for the most part, we knew we were in a recession, this just provides confirmation. The quarter-over-quarter decline is the largest seen since record keeping started in 1947. The positive contributors in the quarter were increases in federal government spending and a reduction in imports, which adds to GDP. The decreases were led by reductions in personal consumption expenditure (PCE), exports, private inventory investment, nonresidential fixed investment, residential fixed investment, and state and local government spending. Somewhat positive news from the announcement was the negative growth of 32.9% was not as bad as the initial estimate of -34.5%.

PCE for the last month of the second quarter was better than expected at 5.6%. The expectation of growth of 5.3% came after significant declines in the previous two months. Personal income, on the other hand, decreased by 1.1% in June. Reductions in stimulus checks due to the COVID-19 pandemic contributed to the month-over-month decrease.

Durable goods orders were better than expected in June. The 7.3% growth seen in the month compares favorably with the expected 6.2%. We have now seen two consecutive months of growth for new orders. In May, new orders grew by 15.1%. The increase was led by transportation equipment orders.

Strength in manufacturing continued in July. The Markit PMI manufacturing number was 50.9. This is lower than the expected 51.3 but still positive. A reading over 50 indicates growth. The ISM manufacturing number of 54.2 was higher than the consensus expectation of 53.6.

A sore spot this week was the ADP employment survey. The report showed payrolls increased by 167,000. This is significantly lower than the expected increase of 1.2 million. Companies using up Paycheck Protection Program funds likely contributed to the significant reduction. Last month, 4.3 million jobs were added to payrolls.

Earnings reports for publicly traded companies continued this week with 77% of S&P 500 companies reporting. So far, earnings are down by 32.1%, which is 23.5% better than expected. Sales are down by 10.4%, which is 1.2% better than expected.

|

|

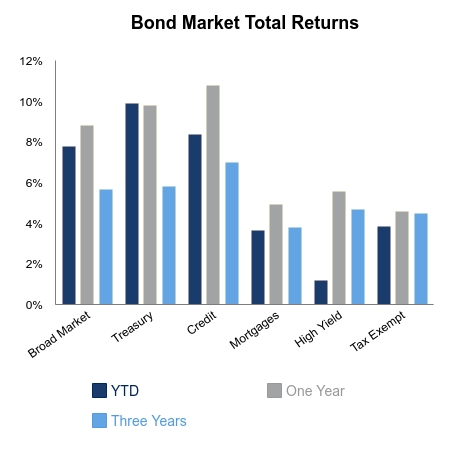

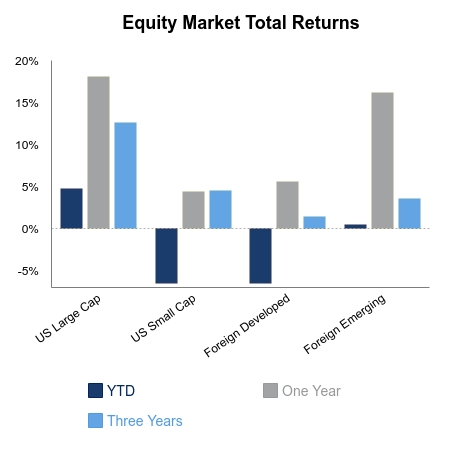

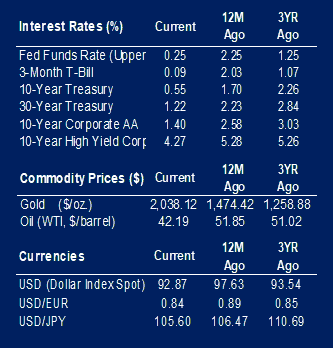

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.