Markets Pullback as AI Themes Lead to the Downside

Key Takeaways

- Technology shares face pressure.

- Sector rotation picks up steam.

- Oil prices hit a five-year low.

Technology shares sold off sharply following 13 consecutive daily advances in the State Street Technology Select Sector ETF. Shares fell more than 6% this week. Broadcom’s conference call wasn’t as clean cut as some had hoped, prompting a 20% drop in share prices this week. Concerns regarding funding for AI-projects, especially those tied to Oracle, led to broad-based weakness in the space.

The S&P 500 finished the week down 2.4%, faring much better than the technology sector as a strong industry rotation transpired. Small caps fared better with a drop of 2.6%, led by the material sector’s gain of 2.7% on the week. Financials and Health Care were also positive on the week. The market is clearly pricing in solid economic growth prospects for 2026.

Delayed October nonfarm payrolls showed a loss of 105,000 due to a large drop in government workers. Private payrolls were up 52,000 but manufacturing was down 9,000. The unemployment rate ticked up to 4.6%, the highest since 2021. Retail sales were also released for October and showed an unchanged reading versus the previous month. Weakness was in autos and building materials, which is excluded in the core number. The core number showed a gain of 0.8%, which was double the market expectation. Sporting goods, department stores, and internet retail all fared well.

Are we only mid-cycle?

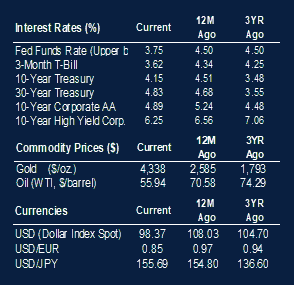

Oil prices have begun to move lower again. Prices dipped under $55 per barrel this week, which is a low dating back to 2021. The national average gasoline price, at $2.90, is also at a five-year low. OPEC+ nations have continued with their supply increases, while U.S. production is at an all-time high. Some potential easing tensions between Russia and Ukraine has helped. If prices are falling due to supply and not demand destruction, then it could be a catalyst to elongate the consumer spending cycle.

The percentage of global central banks cutting rates stands at 84%, a slight drop from 85% in September. To get this high of a number and still have no clear signs of recession should be viewed with optimism. Over the last 30 years, forward equity performance has been strong following a large percentage of central banks easing in the absence of recession. Conversely, weak markets are attributed to emergency cuts to stem falling stock prices and economic output.

|

|

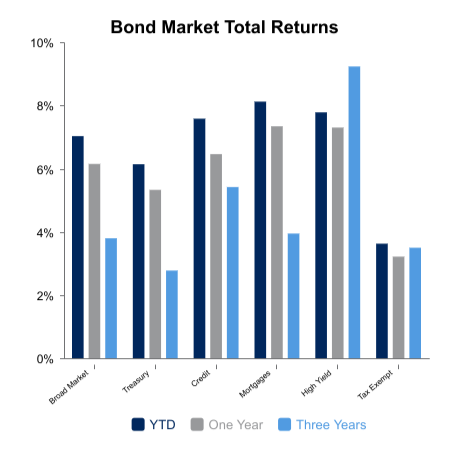

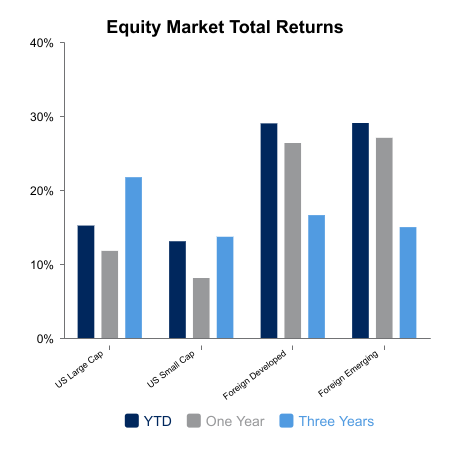

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.