Shortened week of trading has provided some cheer going into close of 2025

Key Takeaways

- Equities continued their year-to-date rise.

- GDP rises while Inflation remains restrained.

- Cooling macro indicators.

Season’s greetings to all! This shortened week of trading has provided some cheer going into the close of 2025.

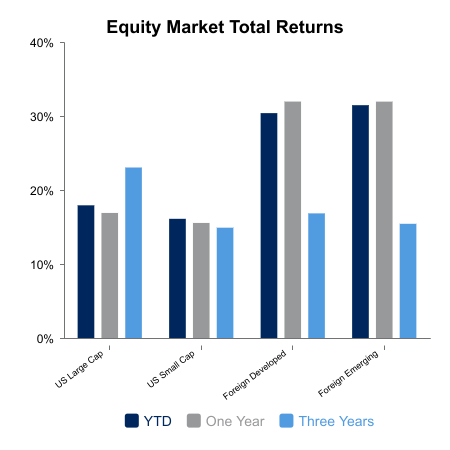

Domestic equities, measured by the Russell 3000 Index, rose 2.7% week‑over‑week (W/W) driven primarily by large cap growth, which advanced 3.9%. Year‑to‑date (YTD), this index has risen 18.4% with growth as the primary driver.

Outside the U.S., the MSCI All‑Country World Index ex-USA (ACWI x-USA) rose 2.0% W/W. ACWI x-USA has surged 32.0% YTD, setting up 2025 to be the first calendar year since 2012 where foreign equities have outperformed domestic equities.

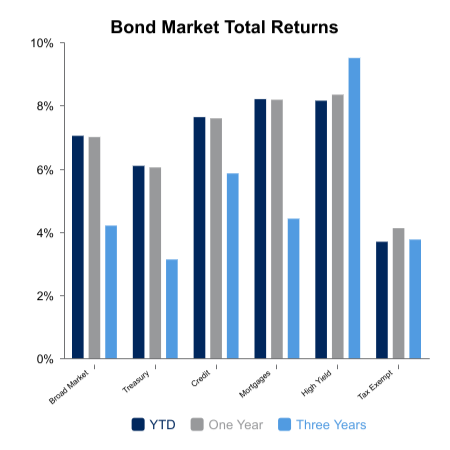

Bonds were flat W/W with no significant moves within the yield curve. Bonds have surprised to the upside, returning 7.0% YTD.

The Bureau of Economic Analysis (BEA) released its first estimate of third quarter U.S. gross domestic product (GDP). BEA estimated GDP expanded at an annual rate of 4.3% versus consensus estimates of 3.0% and greater than the second quarter’s 3.8%. This was the highest reading since the third quarter 2023. BEA attributed the growth in GDP to, “increases in consumer spending, exports, and government spending that were partly offset by a decrease in investment. Imports, which are a subtraction in the calculation of GDP, decreased.”

The Bureau of Labor Statistics (BLS) released its Consumer Price Index (CPI) for November, which increased 2.7% year‑over‑year (YOY), below consensus estimates of 3.1% and September’s 3.0% rise. BLS reported core inflation, CPI ex-Food & Energy, rose 2.6% YOY, the lowest since March 2021. This report should be taken with a grain of salt, as BLS did not report October measures and some from November due to the government shutdown.

The U.S. Census Bureau reported durable goods orders for October fell 2.2% versus consensus expectations for a 1.2% decline and September’s revised rise of 0.7%. Transportation declined 6.5% which was the primary dilutor. Excluding transportation, new orders rose 0.2%. Excluding defense, new orders dropped 1.5%.

The final reading of Consumer Sentiment for December by the University of Michigan came in at 52.9, below consensus of 53.4 and its preliminary reading of 53.3. According to the survey, “Buying conditions for durable goods fell for the fifth straight month,” while “sentiment remains nearly 30% below December 2024, as pocketbook issues continue to dominate consumer views of the economy.”

To all, thanks and have an enjoyable and safe holiday season!

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., London Stock Exchange Group Plc, FTSE Russell, U.S. Bureau of Labor Statistics, U.S. Census Bureau. U.S. Bureau of Economic Analysis.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.