Mixed Economic Signals: ISM Services Improve, Manufacturing Contracts, and Black Friday Surprises

Key Takeaways

- ISM Services improved slightly as rising input cost slowed.

- Bargain buying lifts Black Friday sales better than expected.

- U.S. stocks advance stalls this week following recovery from November pullback.

With 75% of Gross National Product (GDP) coming from services, this week’s improved ISM Services Index posting of 52.6 for November, compared to 52.4 prior, was received by markets as good news for the economy, but underlying figures revealed a contrasting mosaic of data. New orders, a forward-looking indicator of business demand, slowed to 52.9 (versus 56.2 prior), but respondents felt that the government reopening will boost December orders. The prices-paid component that measures materials, goods and services purchased by companies as inputs fell to 65.4 following a 70.0 reading in October.

The ISM Manufacturing Purchasing Managers’ Index was weaker than expected, falling to 48.2 in November from 48.7 in October. This marked the ninth consecutive month of contraction (a reading below 50). This survey showed businesses remain frustrated by supply chain challenges and tariff-related uncertainty. Details of the report show a rise of inventories while new orders, backlog of orders and deliveries all fell during November.

Initial reports show it was a solid weekend for retailers with Mastercard reporting Black Friday sales rose 4.1% over last year, surpassing expectations and beating last year’s 3.4% growth. Despite recent consumer surveys showing a material reduction of confidence and concerns of future inflation, consumers snapped up discounted offers as an opportunity to pull forward buying before prices reset higher.

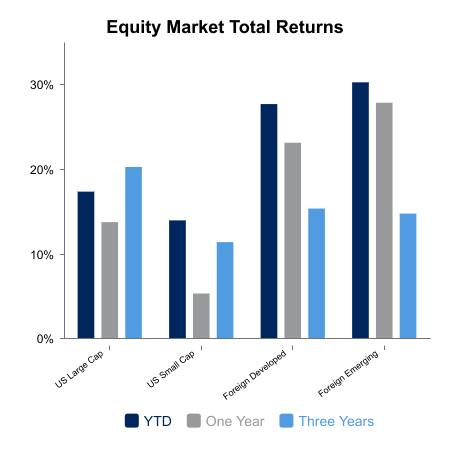

U.S. equity markets continued to bounce back from a late November drawdown advancing by 0.7% this week, adding to a 4.9% rise since that November 20 low. Despite the recent rally, the broad market benchmark represented by the MSCI USA Index remains slightly below its all-time high reached in October. A shift in sector leadership has started to appear as the Healthcare sector, which has been leading over the last three months, underperformed all other sectors this week. As freezing weather crosses the country it’s no surprise that the Energy sector was this week’s stock market leader.

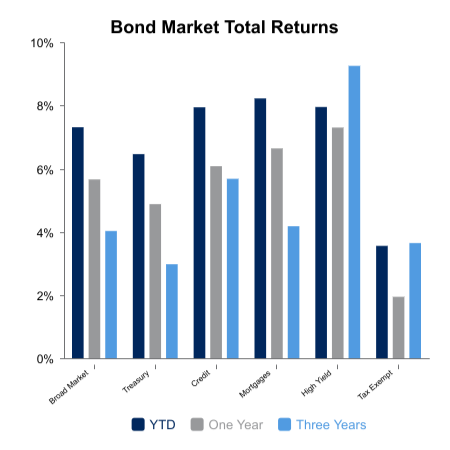

Bond markets declined -0.3% this week, with the U.S. Treasury 10-year yields again moving above the 4.0% level to 4.1%. Market watchers are reluctant to allow an incremental move toward lower bond yields with inflation expected to remain above a 3.0% annualized level over the coming quarters.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.