November was another month where the unemployment rate came in better than expected. The rate of 4.2% shows continued employment gains through 2021. The preannouncement consensus was for unemployment to go down to 4.5% from October’s 4.6%. Gains in professional and businesses services, transportation and warehousing construction, and manufacturing contributed the most to the 0.4% increase.

Labor force participation went up 0.2% to 61.8 in November. This number is 1.5% below the February 2020 number. Since November 2020, labor force participation is up 0.3%. It is unlikely we will see a return to pre-pandemic levels any time soon.

The number of open jobs were up in October with 11.033 million jobs open. This is an increase from 10.602 million in September. October’s reading approaches July’s peak of 11.098 million. The 10-year average for openings is 5.845 million. Companies may have to continue increasing pay to attract workers back into the workforce or robots will need to get a lot smarter.

Growth in earnings was a little lower than expected. Hourly earnings were expected to grow by 5% but only grew by 4.8%. We are still waiting for the Consumer Price Index number to see if wages grew faster than inflation. Despite the growth number being high, we have seen very little growth after accounting for the impact of inflation.

Labor productivity was down significantly in the third quarter. The final reading shows a decline of 5.2%. This is the largest decline since 1960. Hours worked increased by 7.2% and output only increased by 1.8%. Labor productivity is calculated by dividing output by hours worked.

Purchasing Mangers’ Index (PMI) numbers for November were released this week. The composite is at 57.2. This number shows a jump from last month’s 56.5. The services PMI was at 58 and the manufacturing PMI at 58.30. With this index, a reading over 50 shows expectations for economic growth.

The final number for durable orders in October was -0.41%. Transportation orders weighed on the number in the month. Taking out transportation, orders were up 0.5%. This is the third month this year that durable orders have been down.

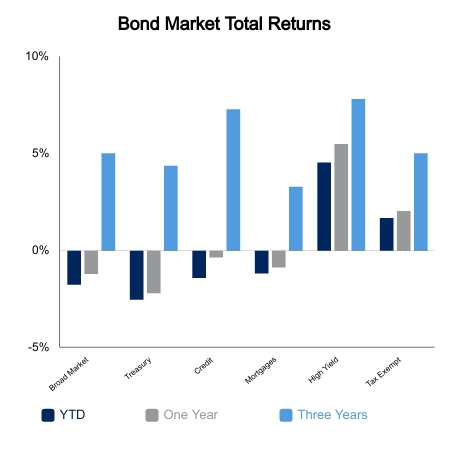

Lastly, it was a strong week for equity markets. The S&P 500 clawed back 4.2% after Omicron variant-related weakness. All sectors in the index were up this week. Energy, real estate, industrials, and materials led performance. These sectors were up over 5%.

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.