Dispersion Surges as AI Fears Expand to More Industries

Key Takeaways

- The AI wrecking ball expands.

- Equity dispersion near record levels.

- Job gains come in better than expected.

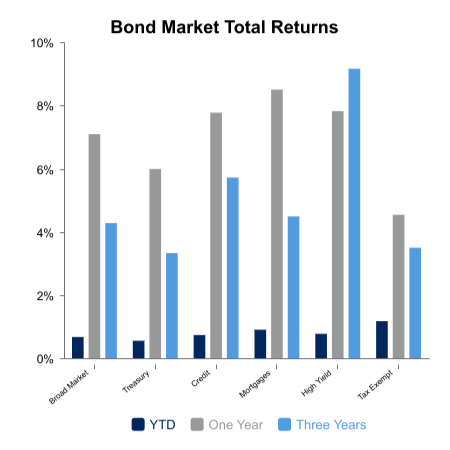

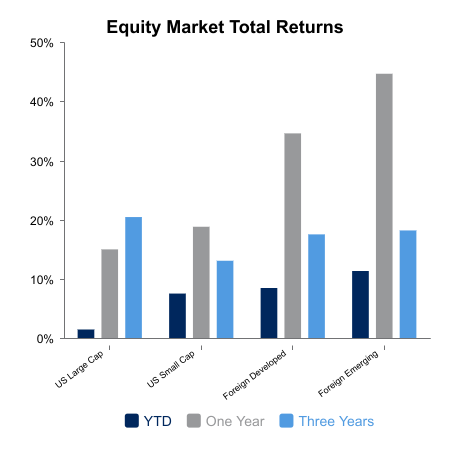

The S&P 500 finished the week up 0.9% amid near record equity dispersion. The NASDAQ lagged with gains of 0.7%. Once again, foreign equities lead the way with gains north of 2% in both emerging markets and foreign developed markets. Fixed income returns were positive as yields moved lower. The S&P 500 is essentially flat over the last month; however, the average stock has moved more than 10%. The variance between average single stock movement and index movement is at its 99th percentile over the last 30 years.

The catalyst this week was the upgrade of several prominent AI models. The release of Opus 4.6 from Anthropic just seven days ago is being hailed for its monumental leap forward. Software names dropped 5% on the news but have traded slightly higher in the last couple of days. This time, selling broadened out to include legal firms, asset managers, and advisory services companies.

Several prominent financial institutions were down 10% on the week. Insurance brokers were down 9% on Monday, their largest single-day decline relative to the S&P 500 since 2008. Legal and data services firms were hit especially hard. S&P Global, known for its credit ratings and index ownership, has dropped more than 26% relative to the S&P 500 Index over the last eight days. This is its largest eight-day relative decline. The last two days have seen real estate services firms drop more than 20%.

Outperforming areas are those that are deemed to be AI-resistant, often tied to real assets of some form. Value has outperformed as has transportation names, infrastructure build out plays, and consumer staples.

Robust job gains highlight the economic calendar

Economic data this week cooled off. Jobless claims ticked higher and job openings showed a large decline from 7.1 million to 6.5 million. Retail sales missed as the core number came in at 0.0% versus the prior month, a miss of 0.4%. The upside was the jobs report that showed a gain of 130,000 jobs in January. Private payrolls fared even better with gains of 172,000, which was more than double the consensus expectation. The report did have a sour note as benchmark revisions said that more than 800,000 jobs that were thought to be created did not actually happen. The recent weakness does come after a strong run of positive upside surprises.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.