Softer CPI Helps Provide Stability to the Equity Market

Key Takeaways

- Equities finish lower for the week.

- CPI comes in softer.

- Fed minutes show hawkish tilt.

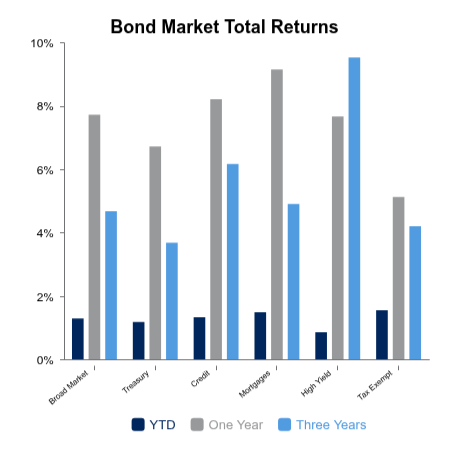

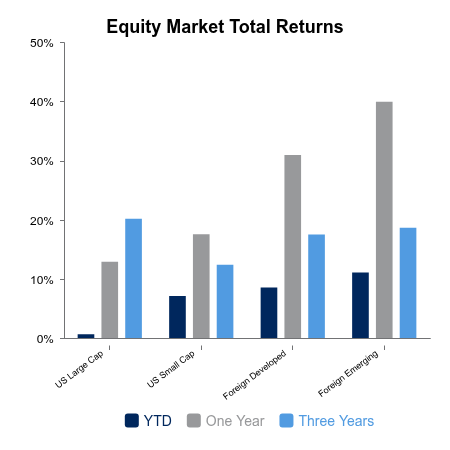

The S&P 500 was down 0.8% for the week. The AI headlines subsided, which helped bring some stability to the oversold industries. Despite this, the general trends of the year persisted with the S&P 500 Equal Weighted Index, developed foreign, and emerging markets all outperforming on the week. The NASDAQ Index continued to lag. Core bonds were up as Treasury yields moved lower in the week.

The best equity industries on year-to-date performance are materials, energy, and industrial products with gains around 20%. Construction, aerospace, and transportation are also faring well. The laggards are business services, consumer discretionary, and technology which are all down on the year. Consumer staples are outpacing discretionary by about 15%, which is usually associated with a weaker business climate. It is unusual to see staples outperform discretionary by such a wide margin while simultaneously seeing cyclical industries lead the market higher. The milestone this month in the consumer staples sector was Walmart becoming the 12th public company in the world to reach a $1 trillion dollar valuation.

CPI comes in better than expected

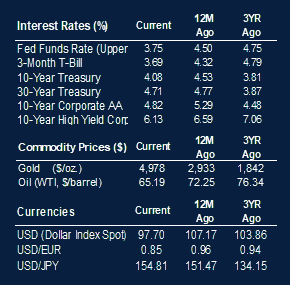

Economic data for the week was highlighted by a better-than-expected consumer price index (CPI) report. CPI came in at +0.2% versus the previous month, which was a tenth lower than expected. Core was in-line, but the unrounded number was 0.26% and helped push bond yields lower. Yields also moved lower on the days when equity prices were down as a flight to safety trade.

Regional manufacturing surveys and industrial production came in better than expected. The release of the latest trade deficit showed a large increase for December, which put a sizeable cut in the Atlanta Fed GDPNow estimate. The estimate for fourth quarter 2025 peaked near 5.5% in January and now sits at 3.0%.

Fed sounds hawkish

The Federal Open Market Committee (FOMC) minutes were released, and the consensus view is they were more hawkish than expected. It noted that several participants indicated they would favor a two-sided description of future rate decisions, reflecting possible upward adjustments. This is the first hint at possible interest rate hikes being relevant in discussions. These minutes, combined with turnover at the Chair of the FOMC, may indicate a sizeable shift underway. Bond yields didn’t move much on the news, possibly taking cues off a soft equity market and potential disinflationary impulse from AI acceleration.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.