Equity Markets Exhibit Near-Term Volatility

Key Takeaways

- Volatility in the equity markets.

- Macro thoughts.

- Fourth-quarter earnings season.

Volatility in the equity markets

U.S. equities experienced a challenging week, falling to near three‑week lows, as big tech stocks underperformed. For the week, the Russell 3000 declined 0.6%, while the MSCI All‑Country World Index ex-USA fell 0.7%. Bonds were not immune to this phenomenon and declined 0.4%.

Trade concerns dominated market sentiment after President Trump announced a 25% tariff on imported chips not used for the U.S. artificial intelligence (AI) industry. Separately, the Supreme Court delayed a ruling on tariffs, adding to uncertainty. Fixed income exhibited this same trait as volatility within Japanese government bonds leached into global markets.

Equity benchmarks stabilized Wednesday given President Trump’s announcement at the World Economic Forum in Davos, Switzerland. President Trump announced a framework agreement with NATO on Greenland, which averted the possibility of new U.S. tariffs on European allies.

Macro thoughts

The National Association of Home Builders (NAHB) released its Housing Market Index for January. The NAHB reported builder confidence for newly built single-family homes fell two points to 37 in January. NAHB acknowledged ongoing challenges within the housing market, commenting that 40% of builders reported cutting prices in January, the third consecutive month the share of builders has been at 40% or higher since May 2020. NAHB reported the average price reduction was 6% in January, up from the prior month while the use of sales incentives was 65% in January, marking the 10th consecutive month this share has exceeded 60%.

The Federal Reserve Board (Fed) reported industrial production for December increased 0.4% and grew at an annual rate of 0.7% during the 2025 fourth quarter. The Fed stated most major market groups advanced in December. Output of consumer goods increased 0.7%, driven by a 1.1% rise in nondurables production which fully offset the 0.7% decline in durables production.

Fourth-quarter earnings season

We’ve entered the 2025 fourth-quarter earnings season, which so far appears to be solid regarding U.S. large cap. Bullish factors include favorable revision and guidance trends.

According to LSEG I/B/E/S, as of last Friday 33 companies of the S&P 500 reported earnings, of which 84.5% exceeded estimates with an average beat of 8.3%. This has resulted in an actual earnings growth rate of 19.0% year‑over‑year (YOY). When blending reported and yet‑to‑report, analysts project earnings will grow 9.0% for the 2025 fourth quarter.

Stay tuned!

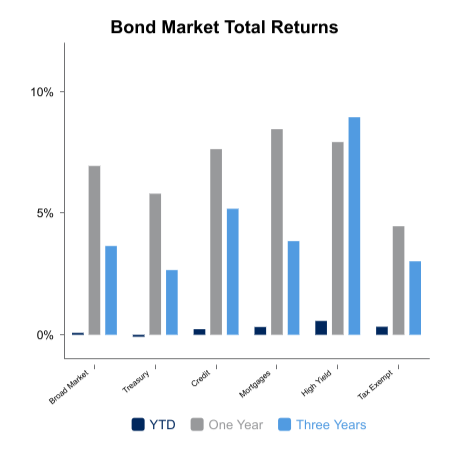

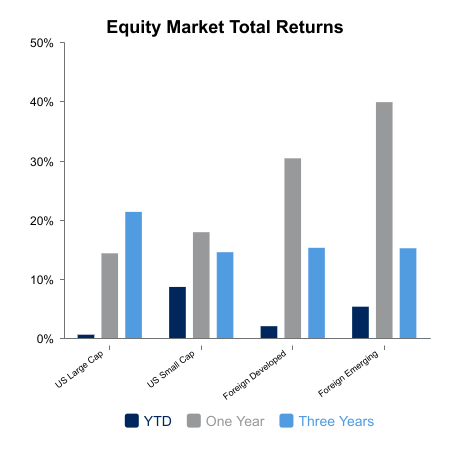

|

|

Sources: BTC Capital Management, FTSE Russell, LSEG I/B/E/S, The Federal Reserve, National Association of Home Builders

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.