Equities turned down as coronavirus fears offered an easy opportunity to take profits. The virus could still be underappreciated given the large number of cases and uncertainty on key attributes. For instance, if the virus can be spread when patients are asymptomatic, then there is the potential for a far-reaching effect with significant impact on global supply chains and travel-related industries. The economic impact would likely be more severe than the analogy to SARS that struck Asia in 2003. After the first case appeared in the United States last week it was no surprise few traders wanted to be long, or buy, over the weekend when new cases could jump. The S&P 500 fell 2.5% on Thursday and Friday but recouped some of the losses to finish the week down 1.4%. Emerging markets were down 3.2%. Bond yields fell in a flight to safety as the 10-year Treasury now yields 1.58%, its lowest level in more than three months.

Initial jobless claims were once again extremely low. The Conference Board Leading Economic Index has stabilized at levels indicative of very weak, but not recessionary, economic activity. New home sales missed expectations but were still up a robust 23% versus the prior year. Core capital goods orders missed expectations by a lot but improved versus the prior year where they were lapping a very weak December 2018 number. This is when uncertainty peaked on a confluence of trade war and federal funds rate hike fears.

The Federal Reserve (Fed) left interest rates unchanged and made little amendments to their statement. The press conference emphasized the desire to get inflation up and thus a higher threshold is needed to raise rates. Again, the market took this as a reason for yields to move lower, while ignoring the fact that higher inflation is a detriment to fixed income returns. The market has made the bet the Fed will try to get inflation higher by cutting rates at the first opportunity but fail to generate inflation. The key repo operations will be extended until April and the Fed has voiced a desire to attempt to back away. It is a popular opinion that the Fed’s repo operations have supported global risk assets in recent months, so there could be plenty of volatility if the Fed does follow through and attempt to back away.

|

|

Contributed by | Justin Carley, CFA, Managing Director

Justin is a Managing Director, providing portfolio management and credit analysis for fixed income strategies. He also manages the firm’s multi-manager portfolio strategies and contributes to the asset allocation framework. Justin has more than 10 years of experience focusing on management, analysis and trading of fixed income portfolios. Previously, Justin was a fixed income portfolio manager at American Trust & Savings Bank. Justin has a bachelor’s degree from Truman State University, holds the Chartered Financial Analyst designation and holds a Fellowship in the Life Insurance Management Institute.

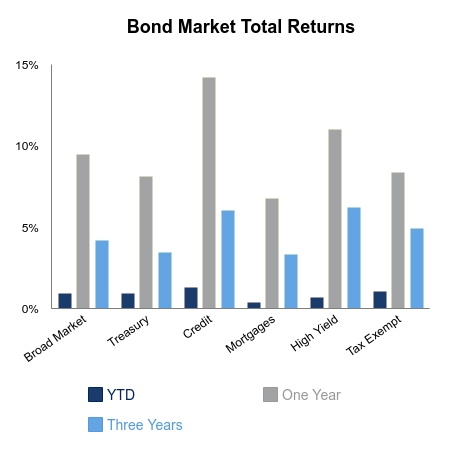

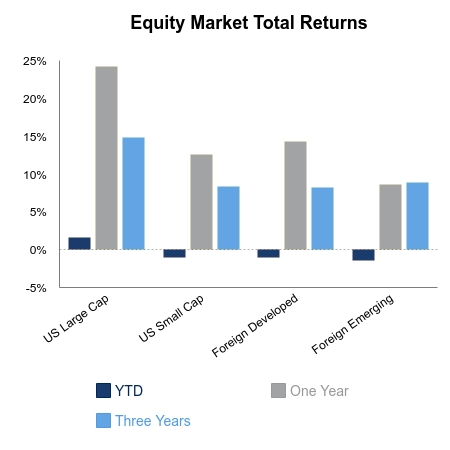

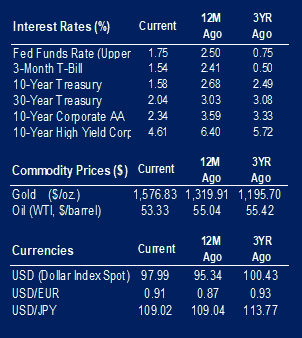

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.