Equities Push to New Highs on Resilient Economic Data

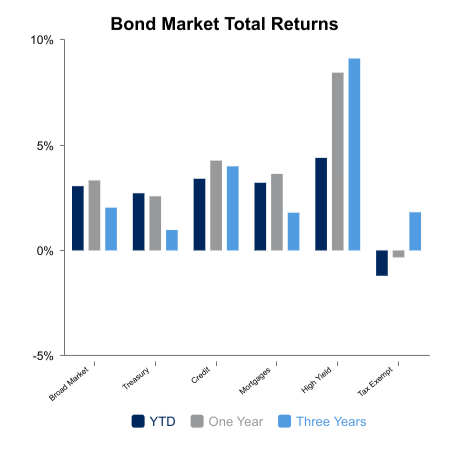

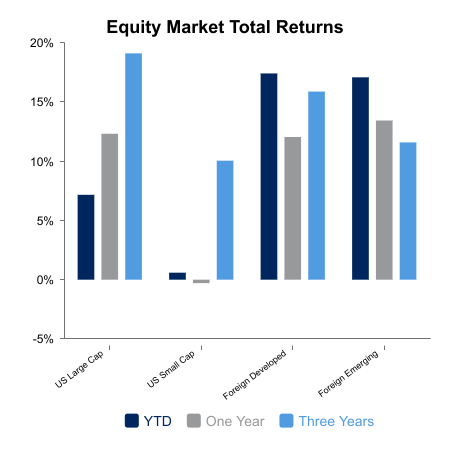

Equities were flat on the week as upward momentum cools off. Momentum may be slowing, but the S&P 500 did hit an intra-day all-time-high this week while the NASDAQ managed to close at a new record. The NASDAQ fared better this week as semiconductors rallied on the easing of some chip restrictions into China. Foreign developed markets were down 2% on the week but maintain their year-to-date relative outperformance versus U.S. market indices. Core bonds were down 0.5% as yields drift higher.

Economic data was generally favorable on the week. Jobless claims ticked back below 230,000. The four-week moving average has gone from 245,000 in June to 229,000, which throws some cold water on those becoming too bearish and extrapolating recent data trends. Some other noteworthy data points are listed below:

- Consumer Price Index (CPI) came in better than expected, as did the Producer Price Index (PPI).

- Some regional manufacturing surveys are starting to show signs of improvement.

- GDPNow currently sits at 2.6% for its second quarter 2025 estimate. The consensus expectation was less than 2% when the quarter began.

Tariffs are back in the headlines as the administration tries to reach a conclusion on many negotiations. It looks as if the levels are going higher than the 10% baseline. Also, aside from major trading partners, countries will be placed into groups with the same rate. Tariffs continue to be a policy tool as Russia had high levies threatened if it doesn’t reach a war deal in 50 days.

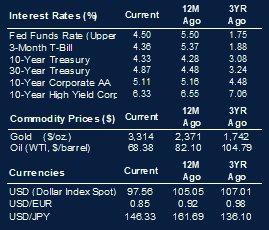

Pressure on the Federal Reserve from the White House continues to gather attention. Talks of Jerome Powell being fired continues to surface, as does the idea of naming a replacement before his term is concluded. This would set the stage for the replacement’s forward guidance to challenge current policy rhetoric. Should this happen, there is a wide range of opinions regarding the immediate and longer-term market impacts.

The market is pricing in one to two cuts in the Federal Funds rate by the end of the year. This would be on par with where we began the year following a five-month stretch when three to four were anticipated. What is different is the expected cumulative cuts through 2026, which sits at two more than the start of the year. This shows the policy skew toward cutting, which has been communicated by several Federal Open Market Committee (FOMC) members. It looks as though any two-month period with subpar growth will be met with interest rate cuts.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.