Strong start to earnings season lifts equity markets

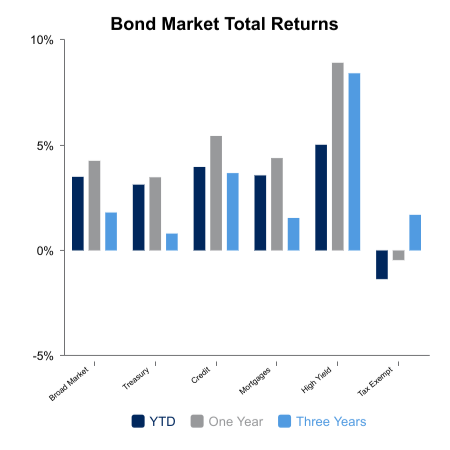

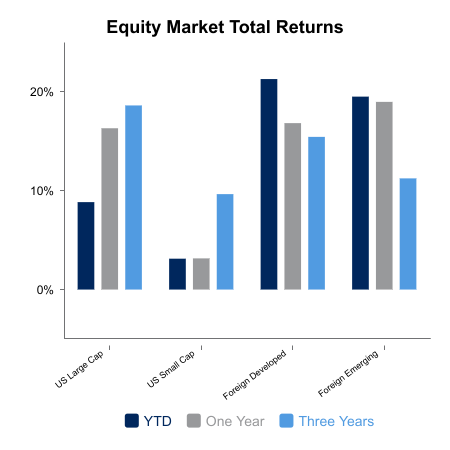

Equities pushed higher on the week as better-than-expected economic data solidified investor confidence in the sustainability of earnings trends. This was highlighted by the 2.5% advance in small cap equities, which outpaced the 1.5% gain in the S&P 500. Regional banks also outperformed on the week. Foreign equities rebounded with strong gains of 3.6%, while emerging markets added 2.1% to round out the global advance. Core bonds advanced 0.4% on the week.

Core retail sales came in better than expected with a 0.5% gain versus the previous month. The annual rate of change has fallen from 5.6% earlier in the year to 4.0% in the latest release. This slowing in the trend has been met with some pessimistic forecasts as the second derivative usually matters more than absolute levels. The 10-year average prior to COVID was 3.3%, so despite the slowing in trend, the absolute number remains solid.

The other big data point is jobless claims falling back down toward 220,000. So much attention is focused on the monthly labor report from the Bureau of Labor Statistics, but this is a lagging indicator. The leading indicator regarding employment is jobless claims. The modest uptick in June has reversed, signaling no imminent danger to the labor market.

- Second quarter 2025 GDPNow estimate sits at 2.4% and has remained above consensus forecasts the entire quarter.

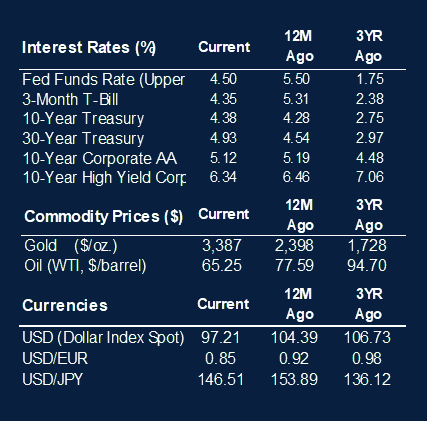

- The Federal Reserve continues to signal an easing bias with some voting members making public comments on their belief interest rate cuts should resume this year.

- The current administration continues to publicly push for lower interest rates.

Earnings season is trying to offset the summer lull in markets. The VIX Index, at 15.2, is at its lowest level since Liberation Day and close to its lowest level this year. Around 15% of the S&P 500 have reported earnings thus far and the beat rate is robust. The market is rewarding positive earnings surprises more than average, while misses are going down less than average. This is what you would expect to see in a strong equity uptrend. The market also remains in gear with the absence of any breadth anomalies as the rally has steadily broadened beyond just large-cap technology. To sum up, the growth in the economy continues to outpace expectations, the Federal Reserve has an easing bias, and there is broad participation in the equity advance.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.