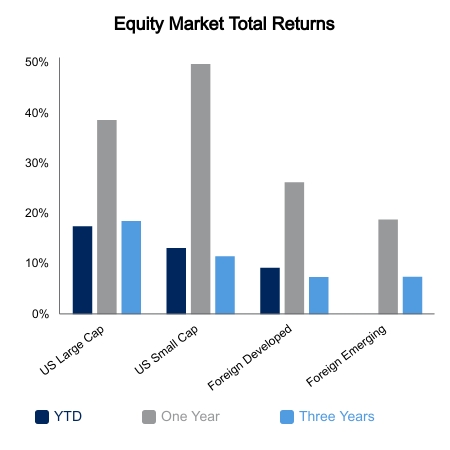

The S&P 500 rallied back this week to again set another high. The index was up 1.0% on the week as large cap domestic equities remain the source of outperformance. The Russell 2000 was down 0.4%. The big news of the week was the crackdown in China regarding several sectors. The market was reminded of the fact that investments in the region are not without risks. The S&P/BNY Mellon China ADR Index was down 9.6% on the week. This dragged down the MSCI Emerging Market Index 3.3%. Thus far the U.S. equity market has remained resilient, potentially aided by a bounce in Chinese stocks late in the week that helped limit the damage.

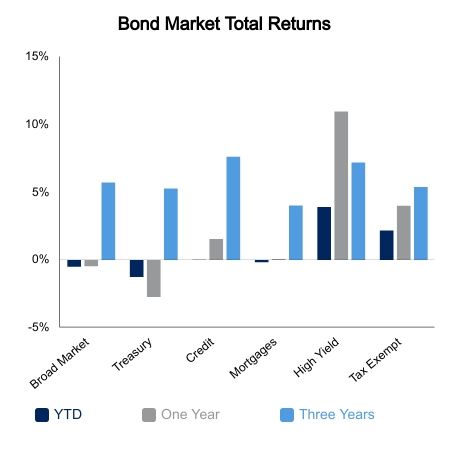

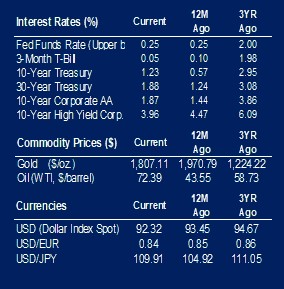

The Bloomberg Barclays Aggregate Bond Index was up 0.4% as yields remain near their recent lows. The 10-year Treasury ended the week at 1.23%. Despite the surprise by many to this low level it remains one of the highest in the developed world. Germany remains the lowest at -0.43%. Should an investor seek maximum yield, they can get over 9% in local currency government bonds in Pakistan, Brazil, and South Africa.

The economic data was a bit behind expectations this week. New home sales were shy of expectations and fell 6.6% versus the prior month. Durable goods core capex orders also missed expectations. Consumer confidence was slightly ahead of expectations, but the real story is the dropping of future expectations versus the present situation. The gap has widened out to levels more emblematic of a mid-to-late cycle economy. It has tended to coincide with negative real wages and bond yields tend to fall going forward.

The Federal Reserve (Fed) convened this week to reiterate their transitory inflation view. The meeting and press release hinted at discussions on tapering but offered more in the way of a dovish tilt with employment goals being a long way off. The market reaction was muted versus historical standards. The increase in virus counts gave the Fed cover to maintain their course despite current high inflation readings. This was anticipated by the market and the Fed did not disappoint. The market is currently pricing in the first Fed Funds hike in 20 months. The last time we came down to these levels in 2013, it took 30 months before the Fed hiked. But it was at this time that the yield curve started flattening in a significant manner.

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.