Catch a Wave and You’re Sitting on Top of the World …

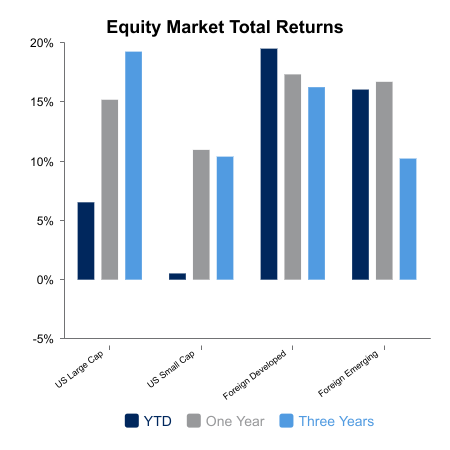

The United States surged during the second quarter, which continued through this past week as the Russell 3000 advanced 2.4%. U.S. small-caps advanced 4.3% for the week while large-caps rose 2.3%.

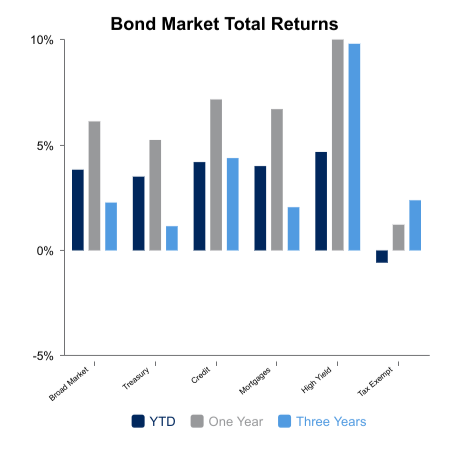

Outside the United States, the MSCI All‑Country World Index ex-USA rose 1.8%. Foreign developed increased 2.1%, while emerging markets eked out a positive gain of 0.9%. Bonds exhibited positive returns of 0.3% for the week.

Tailwinds to broad asset‑class performance were:

- An apparent trade deal between the United States and China as President Trump announced a deal had been penned.

- An easing of geopolitical pressures as the United States mediated a ceasefire between Iran and Israel, which also led to a moderation in the recent uptick of oil prices.

- The perception that a steeper rate cut path may happen soon, given the mixed signals within recent United States economic data.

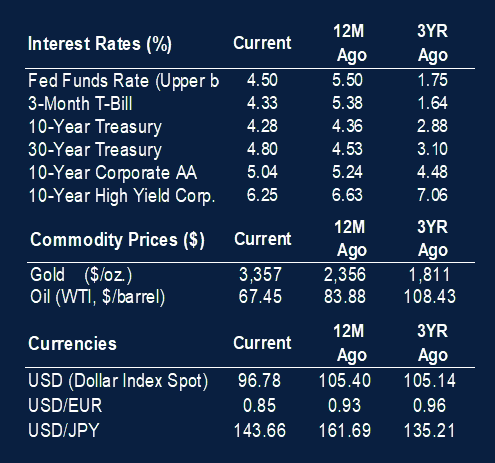

Regarding the last bullet point, New Home Sales for May came in at 623,000. This is the lowest level in seven months, and it is materially lower than consensus expectations of 690,000 and 13.7% below April’s print of 722,000. Elevated housing prices coupled with the current interest rate environment continue to cause headwinds within this industry.

The Bureau of Economic Analysis (BEA) released its third and final estimate for first quarter U.S. Gross Domestic Product (GDP), which decreased at an annual rate of 0.5%. BEA attributed this decrease to “ … an increase in imports, which are a subtraction in the calculation of GDP, and a decrease in government spending. These movements were partly offset by increases in consumer spending.”

BEA also reported a decline of 0.1% in Personal Consumption Expenditures for May versus expectations of a 0.3% increase and April’s reported 0.2% monthly increase. BEA also reported a decline of 0.4% in Personal Income versus expectations of a 0.3% increase following April’s 0.7% increase. This included a 0.6% decline in Disposable Personal Income (personal income less personal current taxes) for the month.

This morning, the Bureau of Labor Statistics (BLS) reported non-farm payrolls advanced by 147,000 versus consensus expectations of 117,500 and May’s increase of 137,000. The unemployment rate dropped to 4.1% from May’s 4.2%. According to BLS, jobs within both state government and health care increased, while the federal government continued to lose jobs.

Second‑quarter earnings season begins in earnest next week – stay tuned.

Wishing all a happy and safe July 4th!

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.