Options Remain

Policymakers at the Federal Reserve did what most expected—nothing. This left the overnight effective borrowing rate around 4.3%. What did make the meeting notable was the “lively” debate that ended with two of the 11 voters dissenting, in favor of a rate cut of 0.25%. 1993 was the last time a meeting had two members vote against the consensus.

Policymakers decided to stay the course based upon two views:

- Labor markets remain stable, so there was no need to ease

- The uncertain impact that higher tariffs may push inflation higher, providing a need to keep monetary policy tight.

This no move policy decision kept their options open to gather more data before the next vote. Currently, the September vote has a 50% chance for a rate cut according to Fed Funds’ futures data.

At 3.0%, second quarter GDP beat economist estimates of 2.7%, a material shift from the -0.5% first quarter reading. Again, it was the net export figure that had a substantial impact on this quarter’s GDP figure, as outsized import activity (negative to GDP) to land goods before tariffs took effect during the first quarter, flipped to net exports (positive to GDP) during the second quarter. Blending the two quarters, U.S. GDP slowed to a 1.25% annualized rate, a percentage point lower than the pace for 2024.

Weakness in the housing market continues as GDP data showed residential investment declined 4.6%, the lowest level since 2022, with spring selling some of the worst figures in over a decade. This confirmed the modest 0.6% rise of new home sales in June reported last week. Inventories of new single-family homes for sale reached the highest level since late 2007, as inventories now represent 9.8 months’ worth of sales at the current pace. The median prices of a new single-family home fell 2.9% from a year earlier.

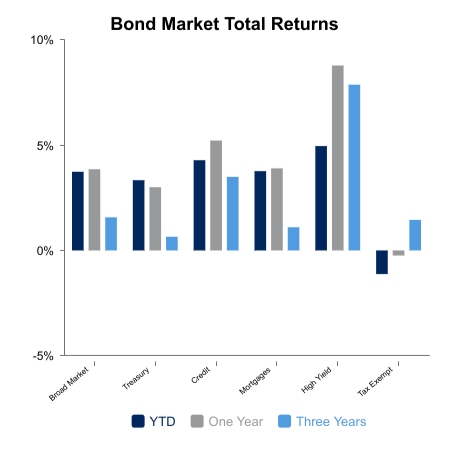

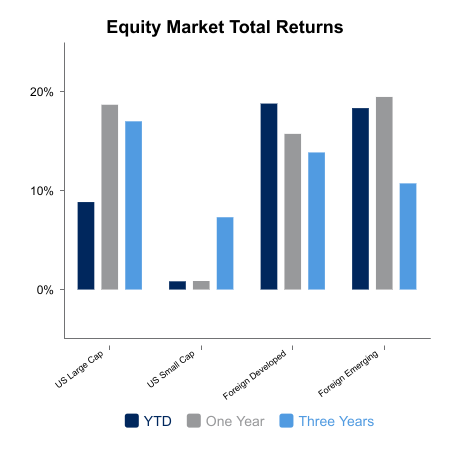

Second quarter earnings have surprised to the upside compared to the tempered forward guidance laid out during first quarter earnings calls that focused on the economic uncertainty following the April tariff implementation. This week, U.S. equity markets were relatively unchanged as the markets waited for earnings releases of leading firms. Following Wednesday’s close, two firms representing 9% of the MSCI USA Index reported large positive upside surprises, setting a high bar for other large companies scheduled to report this week. Bond market returns were 0.3% higher for the week as the 30-year Treasury bond yield declined and corporate spreads continue to tighten relative to treasury securities.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.