No Break this Week for Equity Markets

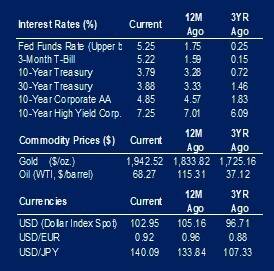

While summer vacation season has started, the equity markets took no break this week as the Russell 1000, an index that measures performance of the broad U.S. stock market, climbed 1.8%. The strong weekly showing brought the year-to-date return up to 14.6%. The same leaders year-to-date contributed the most to this week’s advance as the technology sector (+5.2%) and consumer discretionary (+4.2%) led. Energy stocks were the biggest detractors (-2.5%) as crude oil declined (-5.2%) helping those hitting the road. Bond markets declined (-0.4%) this week cutting into the year-to-date return (+1.9%) as interest rates moved higher across the yield curve with 2-year U.S. Treasury climbing +(0.25%). This climb in rates has primarily been at the 1-to-5-year portion of the yield curve as market consensus is driven by an outlook of a Federal Reserve committed to holding its overnight borrowing rate higher for longer.

Drawing the most focus this week were monthly measures of inflation and the Federal Reserve Board’s meeting to announce the direction of monetary policy. The May Consumer Price Index (CPI) year-over-year (YOY) measure of inflation (+4.0%) declined from its April measure (+4.9%) with energy prices leading the decline. Services, which form 58% of this CPI measure, have been slow to decline over the last year (+6.6%) as prices from three sectors are proving to be sticky: shelter (+8%), car maintenance (+14%) and insurance (+17%). Prices from these segments have not matched the slowing pace of other food and service sectors. The other inflation reading reported by the Bureau of Labor Statistics this week showed the Producer Price Index (PPI) for finished goods declining during the month by -0.3%, but still up 2.8% from a year ago. This lower PPI figure was driven by a drop in goods prices, as easing supply chains, lower commodity costs and shifting consumer demand toward services kept core producer prices in check.

Fed officials held interest rates steady this week after 10 consecutive increases that have raised this key overnight rate by 5% in little over a year. The hold was expected, but the Committee surprised markets with a forecast of two more quarter-point hikes in its economic projections for the remainder of the year. These increases would land the upper range of the rate at 5.75%, signaling policymakers view further tightening is needed to contain price pressures. In Fed Chair Powell’s press conference following the meeting he suggested the Fed passed on hiking at this meeting to allow additional time to examine incoming data and weigh the effects of the changes already made.

|

|

Source: BTC Capital Management, FactSet, Refinitiv (an LSEG company).

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.