Dog Days of Summer

We have formally entered the summer season, and one may expect markets to abate as vacation may now become the front-of-mind issue with investors. We’ve had a holiday-shortened week, but that did not restrain reports on the status of the economy.

The Census Bureau released its retail sales report for the month of May, which surprised to the upside at 0.3% month-over-month. This exceeded consensus expectations for a decline of 0.2% and was in-line with April’s month-over-month increase of 0.37%. It appears that consumer spending remains resilient.

Consumer sentiment appears buoyant as the University of Michigan’s Index of Consumer Sentiment for June came in at 63.9, above both consensus expectations of 60.6 and May’s reading of 59.2. While this is a preliminary report (the final report will be released on June 30), it nevertheless indicates sustained optimism by consumers as inflation continues to decline, putting the Fed on hold for now.

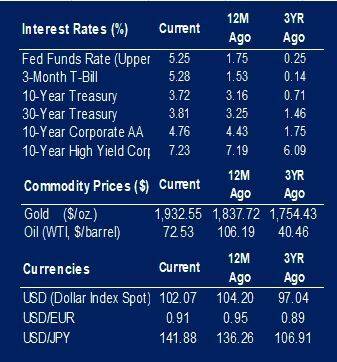

Fed Chair Jerome Powell testified before the House on Wednesday. He will testify before the Senate on Thursday. Key takeaways from Wednesday’s testimony were that nearly all Fed governors believe it appropriate to raise rates prior to year-end and that the Fed’s goal of steering inflation to 2% “has a long way to go,” Chair Powell also noted last week’s dot plot projection for two additional rate increases is “a pretty good guess of what will happen if the economy performs as expected,” although further policy initiatives are anticipated to be in a measured fashion.

Housing continues to exhibit strength. The National Association of Home Builders released its Monthly Housing Index for June, coming in at 55.0, exceeding the 50.0 that was both the consensus expectation and the prior month’s print. Housing starts for May increased 21.7% versus 0.3% consensus and -2.9% for April. Existing-home sales increased 0.2% in May to a seasonally adjusted annual rate of 4.3 million, although sales year-over-year declined 20.4%. Note the S&P 500 Homebuilding sub-sector has increased 41.9% YTD.

Market Overview

Over the last week, bonds grinded out a positive return of 0.7% as yields modestly declined. Year-to-date bonds have advanced 2.78%. Equities cooled globally over the last week, as U.S. equities declined 0.2% while foreign equities fell 0.84%. That said, equities have surprised to the upside year-to-date with U.S. equities up 13.9% while foreign equities have increased 10.26%.

|

|

Source: BTC Capital Management, FactSet, Refinitiv (an LSEG company).

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.