Risk De-escalation, Market Escalation

Both stock and bond markets rallied this past week confident that yet another shock to the economy had passed. The week was steeped in rising risk as a widening Middle East conflict had the potential of cutting off 20% of global oil supply. History suggests most geopolitically led selloffs are short lived unless oil prices continue to rise. Therefore, it was no surprise following a $10 drop for a barrel of oil last Friday that a relief rally in both stock and bond markets followed. Investor concerns that energy inflation would lead to an economic slowdown were set aside by a ramp up of analyst forecasts for positive second quarter earnings growth. With earnings announcements scheduled to start in two weeks, analysts predict cost savings and stabilization of revenues will boost earnings per share in the second half of 2025. Look for our mid-year outlook in the coming weeks for more on this.

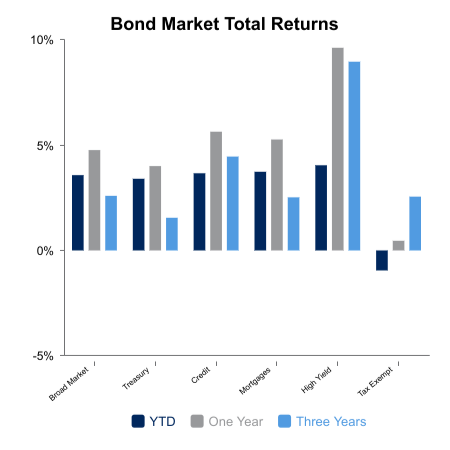

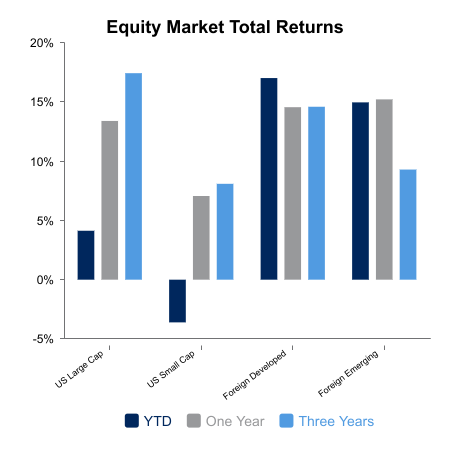

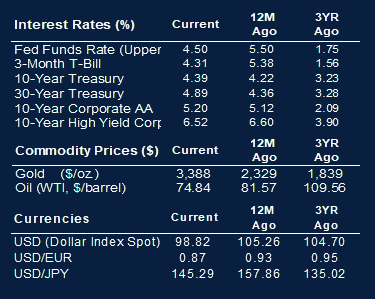

Stocks advanced 1.9% this week, within striking distance of the all-time high reached in February and have advanced 22.7% from the April post “Liberation Day” tariff announcement. Bonds also rallied this week by 0.7% on news of easing tensions in the Middle East, lifting year-to-date returns to 3.6%. Fed Chair Jerome Powell maintained a cautious tone about rate cuts in his semiannual testimony to Congress, noting uncertainty and the inflation risk from tariffs are not yet clearly reflected in the economy. If this risk persists, the Fed is likely to remain steady. Fed officials have recently signaled openness to a cut as soon as July, but markets place only a 27% chance of a cut that soon. Last week’s Fed meeting produced the central bank’s projections for two cuts in 2025 followed by one cut in both 2026 and 2027. Market measures align with the Fed for two cuts in 2025 but see three cuts in 2026, eventually dropping the overnight borrowing rate down to 3.25%.

Consumer confidence in June fell to 93.0 from 98.4 in May, losing much of the gain seen during April. Consumers’ anxiety picked up on concerns of tariff-related price increases likely to kick in late summer and weakened job availability. New home sales fell in May by the most in almost three years as sales incentives have not been enough to overcome affordability constraints. Adding to affordability concerns, building permits for single family homes fell 2.6%, as builders adjust schedules for the rising costs for materials and labor.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.