Equities look past tariffs as the VIX completes a full retracement of Liberation Day spike

Equities rose on the week as investors continue to build optimism that the worst of the tariff impacts have passed. The S&P 500 was up 1.3% as technology names have been driving broader market momentum. NVIDIA has moved higher post-earnings, and large caps continue to outpace small caps. The S&P 100 is up 1.5% year-to-date while small caps are down 5.4%.

Economic data was generally weaker than expected. Both ISM Manufacturing and Non-manufacturing came in below expectations with readings under 50. However, the prices’ paid component was stubbornly high with readings above 68 on both. ADP private payrolls was much weaker than expected and jobless claims have been ticking up of late. This was enough to get yields to take a leg down on the week as economic uncertainty remains elevated.

The policy response trumps everything

There have been some interesting market dynamics that have unfolded over the last year. Since the VIX Index was introduced in 1993, it has only traded over 60 and then below 18 on four occasions. One was the 2008 Financial Crisis that saw the S&P 500 fall more than 55%. The second was during COVID, which was more than 30% straight down for equity indices. The third and fourth times both happened within the last year. The drawdowns were 10% and 20%, respectively, which is significantly less. But even more amazing is that the S&P 500 is up 14.3% over the last year, which is above the historical average.

The Japan stock market crash in August of 2024 saw an immediate policy response. The Bank of Japan (BOJ) reversed course on rate hikes, intervened in currency markets and softened its tone on QT. Potentially more importantly, the Federal Reserve piled on with an oversized 50 basis point cut in the ensuing September Federal Open Market Committee (FOMC) meeting to begin the rate cutting cycle. The Bank of England immediately restarted QE in response to their bond market meltdown in 2022. This year, President Trump reversed course as the S&P 500 drawdown approached 20%.

It appears that the global financial crisis (GFC) days of letting the largest financial institutions fail has been replaced with the COVID mindset, which saw the largest monetary and fiscal response in history. Most market participants are forecasting a range-bound, sluggish equity market over the next quarter. There just doesn’t appear to be a catalyst to drive prices higher. Maybe the catalyst equity markets need is a crisis somewhere in the world?

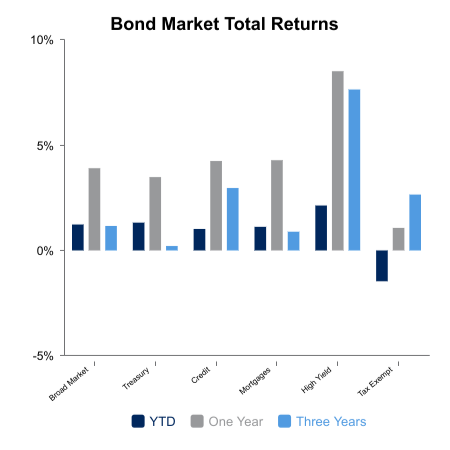

|

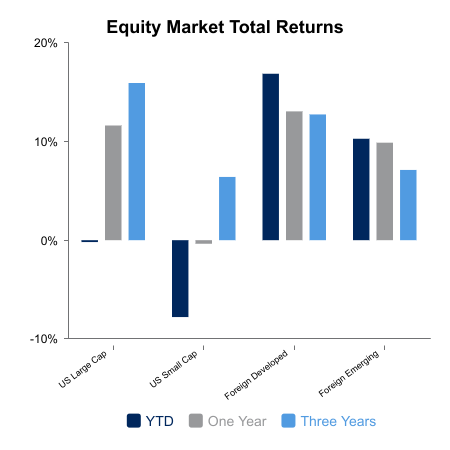

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.