The Fed Stays the Course

Key Takeaways

- Equities decline across the board.

- GDP growth slower than forecast.

- Producer prices register sharp increase.

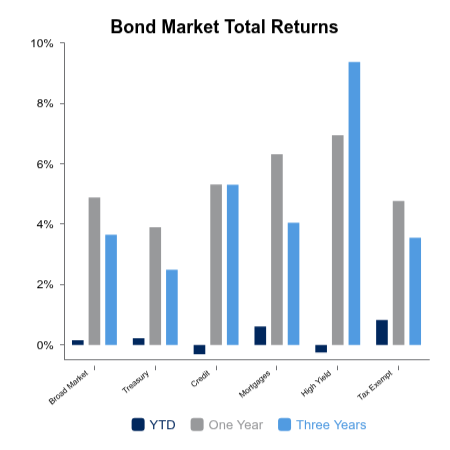

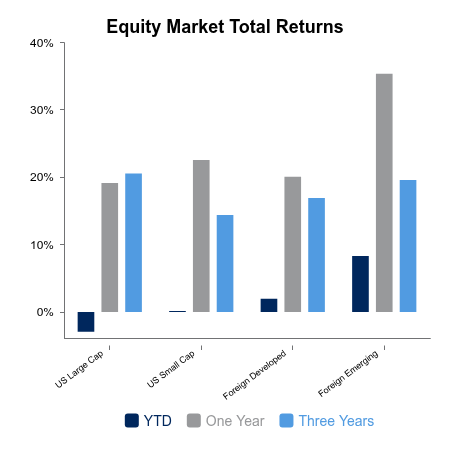

Financial markets were in the red last week as investors were given numerous pieces of economic data to digest while simultaneously monitoring developments from the Middle East. Bonds were only marginally lower with broad market indices returning -0.3% for the week. On a year-to-date basis, bonds are essentially flat. Equities fared worse than their fixed income counterparts for the week as the Russell 3000 Index of U.S. equities declined 2.3%. While value stocks have delivered a positive return of 2.3% year-to-date, they were also in the red for the week along with international equities, as measured by the MSCI EAFE Index, which declined 0.8%.

While economic growth for the first quarter may come in slower than previously projected, corporate earnings are still expected to show double-digit growth. FactSet is currently projecting a year-over-year first quarter growth rate of 11.6% for the companies comprising of the S&P 500 Index.

Another prominent economic announcement for the week was the Federal Reserve’s (Fed) decision to leave the Fed Funds rate unchanged from the current level. The Fed cited an expanding pace of economic activity in support of their decision despite a sluggish labor market. Given the Fed’s comments, the prospect of future cuts to the Fed Funds rate have been pushed into next year.

On the labor front the latest JOLTS (Job Openings and Labor Turnover Survey) data was released with a figure of 6.9 million job openings, the largest monthly increase since October 2024. This figure was meaningfully higher than consensus expectations and represented a substantial increase over the prior period’s result. Despite the strong result, the number of unemployed continues to exceed the number of job openings.

Another piece of data that came in stronger than forecast was the Producer Price Index (PPI). In February, the measure increased 0.7% versus a consensus expectation of 0.3%. Going forward, inflation measures such as the PPI will be closely evaluated as to the impact of higher oil prices currently flowing through the economy.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.