Equity Markets Shrug Off Extraordinary Bond Market Volatility

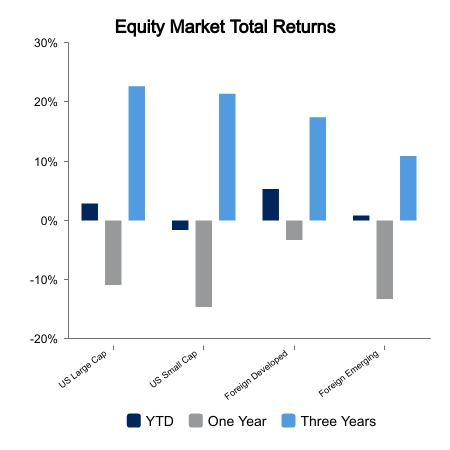

The S&P 500 was up 1.2% on the week as strength in large cap technology overcame weakness in smaller cyclical stocks. Cyclical stocks have been weak of late as global bank failures raise concern about the future growth trajectory. Investors appear to be viewing large cap technology as better insulated and have bid up prices in recent days.

Sunday Night Drama

It was the second straight week where investors where intently focused on Sunday night markets. Policy makers fear any lingering uncertainty in the markets, so they force distressed situations through over the weekend to calm investors before Asian markets open. This time the 166-year-old Credit Suisse, a global systemically important bank, was on the verge of collapse. It was forced into UBS over the weekend with shareholders receiving less than $1 per share.

U.S. equity markets appreciated the resolution, but European banks fell on the news due to Swiss lawmakers wiping out contingent convertible bonds while paying out equity holders. This goes against the common law hierarchy of payments. It was allowed because the bonds had a loophole that allowed Switzerland to change the laws, which they did overnight. This is a key source of capital for European financials and there was fear this entire source of funding would be eliminated. This fear was alleviated as countries came out and said that these bonds would rank above equity in nearly all other jurisdictions.

Fed Raises 25 Basis Points as Bonds Begin to Price in Recession

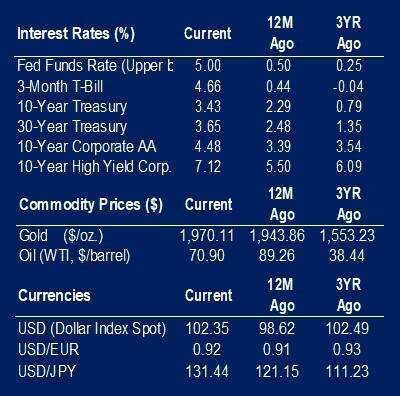

The Federal Open Market Committee raised interest rates 25 basis points this week to an upper limit of 5.0%. They forecast one additional hike this year and no cuts. On the contrary, the bond market is pricing in 2-3 cuts by year end in what some are saying is the largest gap between Fed forecasts and market forecasts since the “dot-plot” was created in 2012.

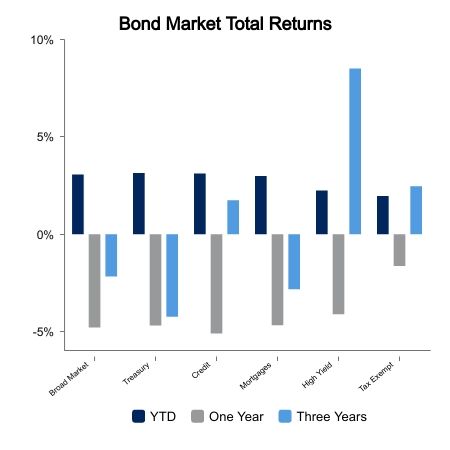

This month, bond market volatility, as measured by the MOVE Index, surpassed the Asian financial crisis of 1998 and the COVID crisis of 2020. Only the Global Financial Crisis saw a slightly higher reading on bond market volatility. The other key theme in the fixed income space is the steepening of the yield curves. This is normally the timeliest aspect of yield curve inversions. Once the curves steepen it is often a sign that the recession is close at hand. In just over two weeks the spread between the 5-year and 30-year Treasury went from being inverted by 45 basis points to being positively sloped by 20 basis points. It is the largest increase over this time span since 2001.

|

|

Source: BTC Capital Management, Bloomberg LP, FactSet, Refinitiv (an LSEG company).

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.