Higher-than-expected inflation was a large market-influencing concern this week. In April, prices increased by 4.2% year-over-year, as measured by the Consumer Price Index (CPI). The increase is the largest 12-month rise since September 2008 when prices grew by 4.9%. The expectation was for growth of only 3.6%. The increase was led by strong growth in energy, which was up 25.1% in the period. Excluding energy and food, CPI was up 3%, which is still strong. The largest increase excluding energy came from used car pricing, which is up 21%. Over the month, used car prices were up 10%. This is the largest increase since measurement of the series started in 1953. Month-over-month, headline CPI was up by 0.8% and Core CPI was up by 0.9%.

The discussion now surrounds whether increased prices will persist or if they are just transitory. Inflation generally negatively impacts investment returns. The inflation announcement contributed to equity markets, as measured by the S&P 500 Index, being down 2.46% this week. The decline was led by the consumer discretionary and information technology sectors, down 4.97% and 3.78%, respectively. All sectors but energy were down this week.

This dour one-week performance follows a strong earnings season. A little over 90% of S&P 500 companies have reported earnings and sales. Earnings from the reported companies grew 49.44% from a year ago, which is 22.5% better than expected. Sales grew by 10.37%, which is 3.85% better than expected. Judging by market performance, it looks like a lot of the growth was built into company valuations.

Another drag on markets this week was the disappointing Nonfarm Payroll numbers. Employment was expected to increase by 975,000. What we saw instead was an increase of only 266,000. The lower-than-expected number contributed to the unemployment rate staying at 6.1%. A decrease to 5.8% was anticipated. The industry with the most significant increase in jobs was leisure and hospitality. This comes after a sharp drop in service worker employment through the COVID-19 pandemic.

Hourly wages increased by 0.7% in April. The increase was offset by the above referenced month-over-month CPI number of 0.8%. Real average wages were virtually flat after the offset. This number shows the potential impact of inflation on wages. Year-over-year, hourly wages are up 0.3%.

Oil prices, as measured by the WTI Crude Oil index, were down 1% after two consecutive weeks of greater than 2% growth. Prices are expected to increase as economic activity picks up.

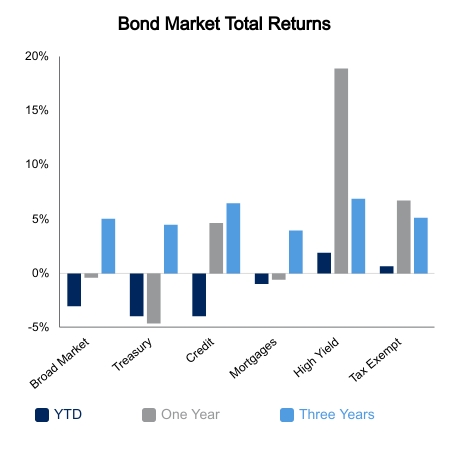

|

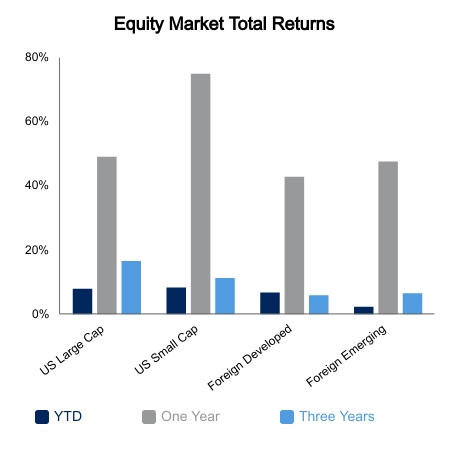

|

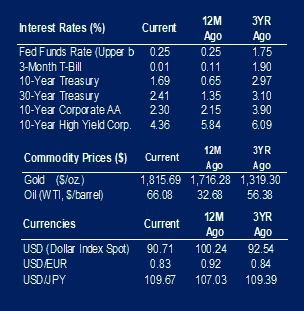

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.