The door slowly closes on another earnings season as 90% of S&P 500 companies have reported negative earnings and sales growth for the first quarter of 2020. Earnings have declined by 12.2% for the quarter, which is 3.1% better than expected. The decline in earnings growth was led by shared drops in the earnings of consumer discretionary and financial companies. Car companies were among the biggest detractors from growth within the consumer discretionary sector. Banks and consumer financial companies were the significant detractors in financials. Sales declined by 1.7%, 1.0% worse than expected. These results are meaningfully negative. The pessimism continues as we navigate the second quarter, as earnings and sales growth numbers are expected to be even worse.

We saw a significant increase in April’s hourly earnings growth numbers. Month-over-month, earnings grew by 4.7%. Year-over-year, they were up by 7.9%. Unfortunately, the comparison over the previous month is not necessarily fair. COVID-19 has had a larger impact on the employment of workers at the lower end of the wage scale. This increase in low wage unemployment has led to an artificial increase in the hourly earnings growth rates as the weighting to higher wage earners increases.

The U.S. unemployment rate is the highest it has been since this number has been tracked. April’s reading of 14.7 million gives a strong indication of the devastating impact of COVID-19 on people and the economy. There is little solace in the reading for the month being better than the expected rate of 16%.

3.169 million additional people filed for unemployment insurance the week that ended on May 2. This is 169,000 more people than expected.

We saw some marginally positive economic news this week. The preliminary first quarter productivity number was better than expected. The announcement of a first quarter decline of 2.5% was better than the forecasted decline of 6.0%.

Companies reduced inventories by less than expected in March. There was a contraction of 0.80% compared to the expected 1.0%.

Energy continues to have a significant impact on inflation numbers as seen in the April Consumer Price Index (CPI) numbers. Year-over-year, core CPI, which excludes food and energy, grew by 1.4%. Including food and energy, CPI grew by an anemic 0.30%. The expectation is for a continuation of flatness for price levels in May.

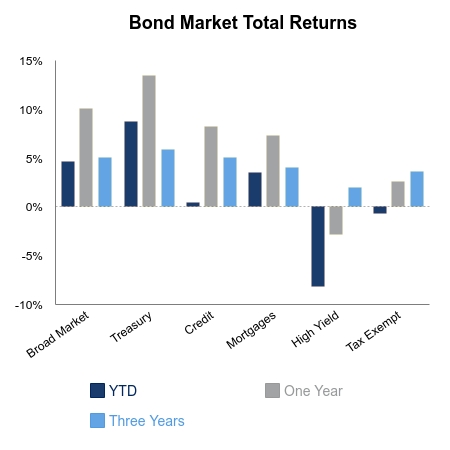

|

|

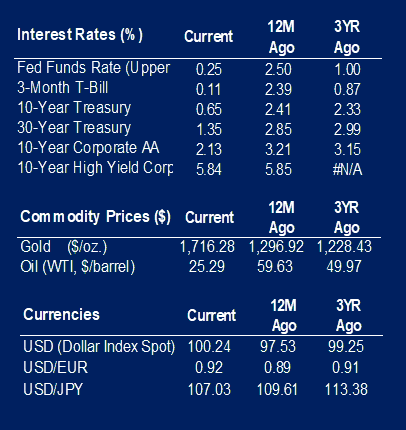

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.