Fixed income markets moved to the forefront this week with extensive commentary regarding the auction of 20-year bonds by the U.S. Treasury. The issue sold at a yield of 5.047%, slightly higher than the 5.035% yield for a 20-year issue that was in place just before the deadline for bids was reached. This differential in yield led to the observation that the auction was weak, as the differential between auction yield and actual yield at the time of the auction was above the historical average.

This scenario was interpreted as a sign that investors are growing more wary about the significant budget deficits in the U.S. Amplifying this angst is the passage in the U.S. House of Representatives of a budget bill that, per the Congressional Budget Office, potentially adds up to $3.8 trillion to the government’s level of outstanding debt.

Offsetting some of the concern regarding the 20-year auction was the fact that international investors bought the majority of the issue signaling continued confidence in the quality of U.S. Treasury debt.

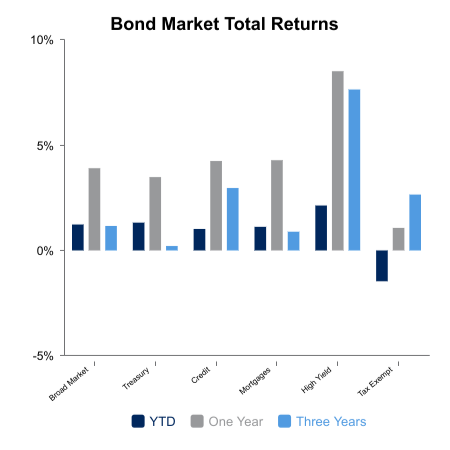

Interest rates did move higher over the course of the week as the 10-year U.S. Treasury issue saw its yield move from 4.54% to 4.60%. The move higher in yields translated into a weekly return of -0.2% for broad market indices. Despite the negative result for the week, the bond market still enjoys a positive 1.2% return year-to-date.

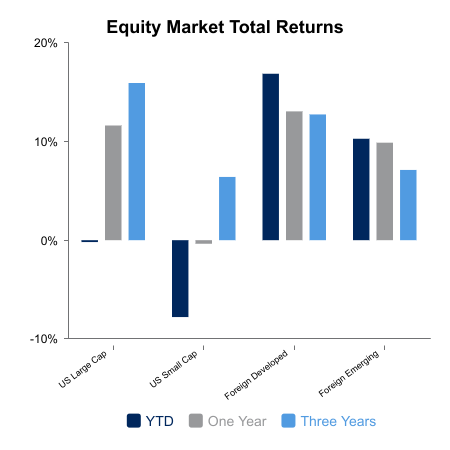

U.S. equity markets also experienced a move lower for the week with the Russell 3000 Index of domestic companies returning -0.9%. Growth and value indices were virtually equal in their weekly returns but over the month-to-date and quarter-to-date periods growth stock performance has far exceeded the results generated by value stocks. This strength from the growth sector has been the most significant contributor to the market rally that has taken place since the low established for the Russell 3000 on April 8.

Globally, international equities continued to outperform their domestic counterparts as the MSCI EAFE Index returned 1.2% for the week.

On the economic front the NAHB Housing Market Index was released and registered a decline of six points, from 40.0 to 34.0. This was the lowest reading since December 2022 and reflects the concerns of builders as they enter the spring home buying season. One caveat to this reading is that it reflects builder sentiment prior to the tariff reduction announcement between China and the U.S.

Next week’s economic releases will include the initial revision of first quarter GDP. Currently the result is anticipated to be unchanged from the original estimate of -0.3%.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.