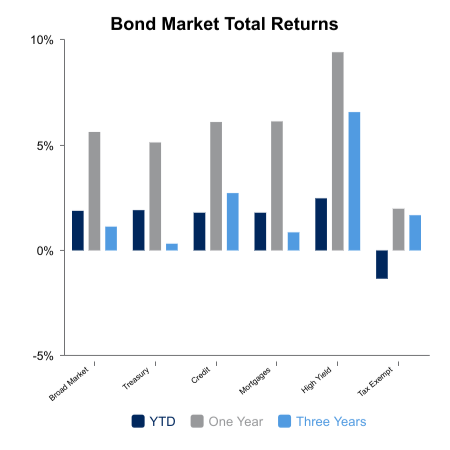

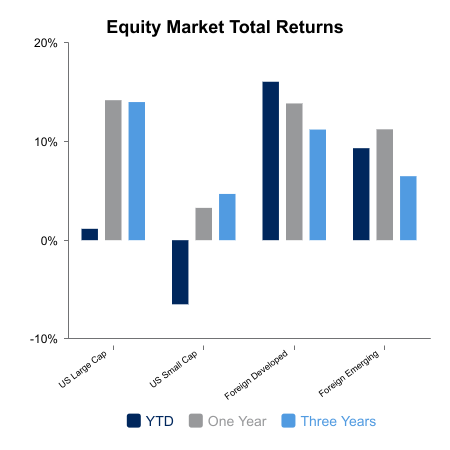

Equity markets rose during a shortened trading week as investors adopted a “risk-on” mentality given positive economic releases and solid corporate earnings results. The S&P 500 Index gained 0.8%, while the Nasdaq Composite rose 1.2%. The Magnificent 7 climbed 2.3%. Small caps climbed 1% for the week. Bond indices rose 0.6% during the week.

Trade Talks with the European Union Improve

Earlier this week, the White House administration announced it would be delaying a previously proposed 50% tariff on goods from the European Union, as trade talks between the two regions were said to have improved over Memorial Day weekend. The U.S. imports a significant amount of goods from European countries such as Germany and Ireland. The European Union initially approved new tariffs on American imports such as soybeans and other agricultural products in response to the recently implemented tariffs initiated by the White House earlier this year.

Consumers Continue to Buoy the Economy

Despite persistent high interest rates, the U.S. consumer continues to provide major support to the overall economy. The Conference Board’s Consumer Confidence Index for May came in significantly higher than forecasted, with much of the positive sentiment based upon developments in the U.S./China trade negotiations. This reverses the trend from the prior five consecutive months which had seen a decline in the Consumer Confidence Index.

Other economic metrics recently released show a general positive trend. Markit’s PMI indices for Manufacturing and for Services for May came in higher than expected as the two segments of the economy continue in expansion mode.

Additionally, new home sales for the month of April reached a three year high as home builders discounted prices to garner more buyers amid relatively high mortgage rates and uncertainty regarding building material prices.

Strong First Quarter Earnings Season Results

With first quarter earnings season essentially in the books, results appear to be very solid and generally broad based. 95% of the S&P 500 companies have reported thus far, with approximately three quarters beating analysts’ expectations. Year-over-year earnings growth for the first quarter is forecasted to be 14%, higher than originally forecasted. All sectors saw year-over-year growth in earnings except for Energy and Real Estate. However, year-over-year earnings forecast for calendar year 2025 is currently 8.4%, lower than forecasts earlier in the year as uncertainty continues to linger regarding the impact of potential tariffs. The Health Care and Information Technology sectors are expected to provide leadership with regards to earnings growth.

Foreign Markets Outpace U.S.

Foreign developed equity markets continue to outpace U.S. equity markets thus far, year-to-date. Various key European indices such as those in the U.K. and Germany have gained approximately 20% year-to-date while U.S. large cap stocks are essentially flat. Flows into global equity funds have also recently increased as investors rotate into other regions, specifically markets such as Western Europe.

Next week’s economic releases will include the initial revision of first quarter GDP. Currently the result is anticipated to be unchanged from the original estimate of -0.3%.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau, Markit

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.