Equity Markets – Tech Falls While Broad Market Gains

Key Takeaways

- Third quarter earnings results very strong

- A.I. buildout continues its momentum

- U.S. government shutdown ends

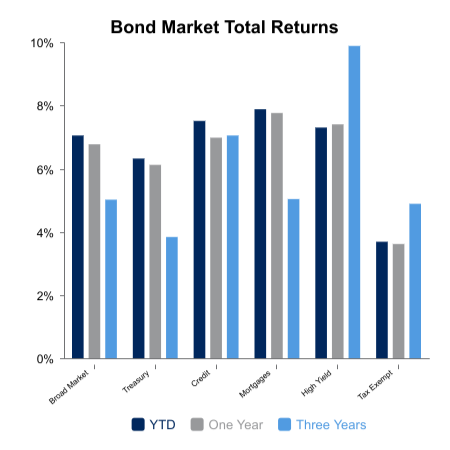

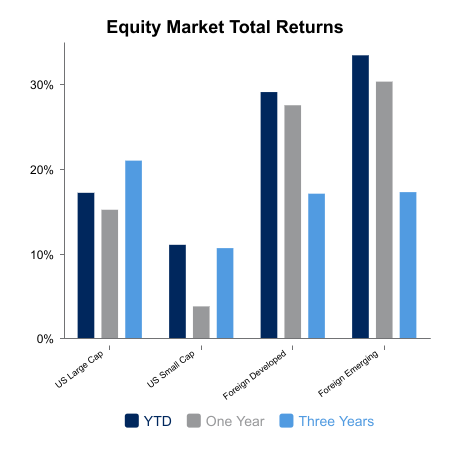

Equity markets were mixed during the week as tech stocks sold off on fears of frothy valuations while the broader market rose. The S&P 500 Index gained 0.8% while the Nasdaq fell 0.4%. The Magnificent 7 dropped 1.6%. Small caps climbed 0.7% for the week. Bond indices rose 0.5% during the week.

Government Shutdown Ends

This week the House and Senate approved a funding bill that ended the longest government shutdown in U.S. history. The bill keeps government funding at the same levels as fiscal year 2025 through to January 30, 2026.

Due to the government shutdown, economic releases were very limited. This week the NFIB Small Business Optimism index for October came in at a six-month low as small business owners cited labor availability and quality as the primary source of uncertainty.

Third Quarter Earnings Results Very Strong

Third quarter earnings results have seen very strong results. Almost 90% of companies in the S&P 500 have reported, with 82% of companies beating analysts’ earnings expectations. Sectors such as Financials and Industrials have joined the Technology sector in providing leadership with regards to earnings growth. Year-over-year third quarter earnings growth is expected to finish at 16.8%, much higher than was forecasted at the beginning of earnings season. Calendar year 2025 earnings growth has been increased to 12.5%, while calendar year 2026 earnings growth is currently forecasted at 13.8%.

A.I. Buildout Continues

As companies report third quarter earnings, there has been commentary regarding the buildout and integration of A.I. across a broad swath of companies and sectors. As corporations look to integrate A.I. into their operations, those companies that provide the hardware and infrastructure for this implementation have benefited immensely as demand continues to grow. The U.S. government has also begun to implement A.I. technology, specifically regarding defense operations. This has benefited companies such as Palantir Technologies and Bigbear.ai, who recently have won contracts to provide the government with A.I. related services.

Returning to a More “Concentrated” Index

With the recent tech rally, the S&P 500 has become concentrated yet again with the top 10 stocks representing approximately 40% of the weight in the benchmark. Since the end of August of this year to the end of the first week of November, the Magnificent 7 has gained approximately 12.8%, while the S&P 500 has risen only 4.4%. The equally weighted S&P 500 was essentially flat during the same time period, illustrating that the majority of stocks in the broad index have not seen gains.

Foreign Markets Outpace U.S. Due to Multiple Expansions

Foreign markets have outpaced U.S. markets year-to-date with emerging markets outperforming foreign developed markets. When looking at the source of gains, foreign markets have relied more on an increase in the price-to-earnings (P/E) multiple as opposed to a significant increase in earnings which drove indices higher. Within the U.S., even though valuations are at the high end of their historical range, the gains seen in the markets have primarily been attributable to earnings growth.

Despite the outperformance year-to-date, flows to foreign funds have recently seen declines as investors are wary regarding the continued increase in multiple expansion.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., London Stock Exchange Group Plc, FTSE Russell, S&P Global, Inc., ADPResearch, Institute for Supply Management.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.