The Economic Data Spigot Reopens

Key Takeaways

- Data releases will impact further rate reductions

- Inflation stability

- Equities move lower

With the ending of the government shutdown last week, we will soon begin seeing a plethora of economic data releases. Later this week we will get employment data for the month of September including changes in payrolls and an updated unemployment rate. Next week’s releases will include data on GDP for the third quarter. Currently the Atlanta Federal Reserve Bank’s GDPNow forecasting model indicates a robust 4.2% rate of growth for the third quarter.

FOMC Minutes Highlight Lack of Government Data

In this week’s release of the minutes from the Federal Reserve’s Open Market Committee (FOMC) meeting held in late October it included comments that their decision-making process was impacted by the lack of economic data available due to the government shutdown. The Fed often cites their dependency on data as a key variable in their decisions related to monetary policy including prospective additional cuts to the Fed Funds rate. Prior to the next meeting of the FOMC the committee will have the opportunity to have updates on inflation and employment, two of the key variables in their mandate to support stable prices and full employment.

Alternative Inflation Data Show Inflation Stability

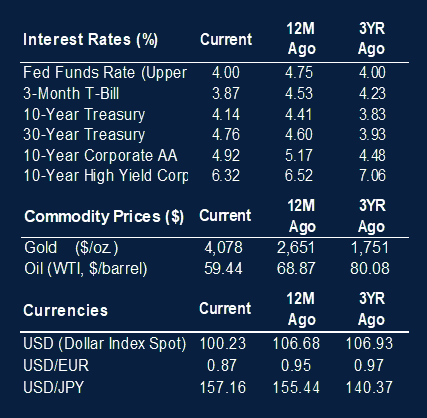

While official updates on inflation are sparse a proxy for the Consumer Price Index is available and it indicates inflation is currently little changed from prior reports. The Federal Reserve Bank of Cleveland makes available the results of its “inflation nowcasting” model. Currently it estimates that consumer prices were increasing at a year over year rate of 2.96% in October. This rate is virtually equal to the level of 3.0% reported for the month of September.

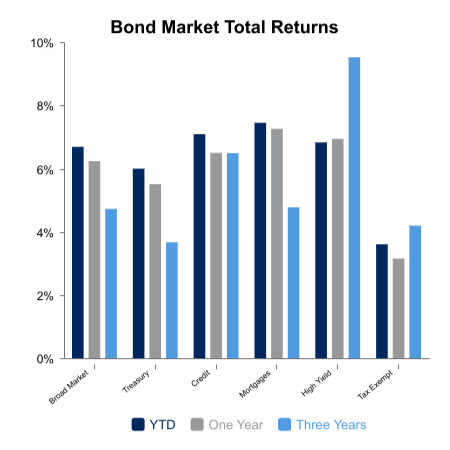

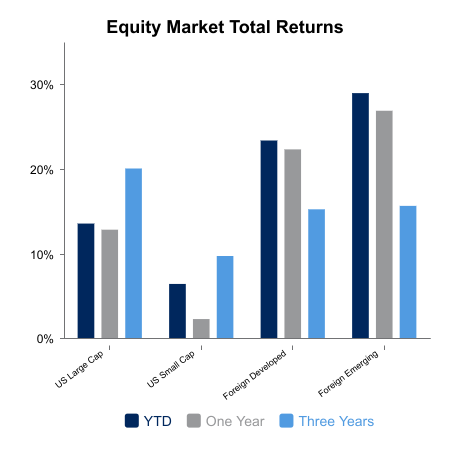

Equities and Fixed Income Returns Weaken

Both equities and fixed income moved lower for the week. The decline for bonds was marginal as the broad market returned -0.3%. Despite the slight negative for the week the asset class continues to do well year-to-date with a return of 6.7%.

Equity declines occurred across the board with all segments (large-cap, small-cap, growth, value, international) posting negative returns. Investors’ concerns about the sustainability and momentum of the AI buildout combined with the declining probability of a Fed Funds rate cut next month contributed to a risk-off mentality. Currently futures markets indicate only a 29% probability that the Fed moves forward with another Fed Funds rate reduction at their next meeting which occurs on December 9 – 10.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.