Equities Rally Amid Rotation Trade

Key Takeaways

- Equities bounce back sharply

- The Fed guides to a cut in December

- Economic data remains mixed

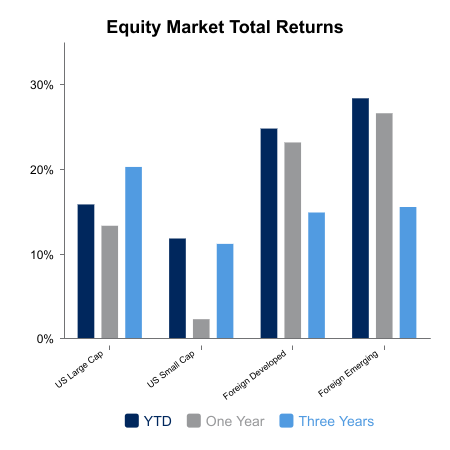

Equities gained 2.5% on the week as a major rotation unfolded. Data center momentum names remain well off their highs while cyclical sectors staged a strong rally. Small caps advanced 5.7% on the week while the NASDAQ 100 lagged with gains of 2.2%. Foreign markets lagged by tracking the U.S. lower on down days but failed to follow suit on the up days.

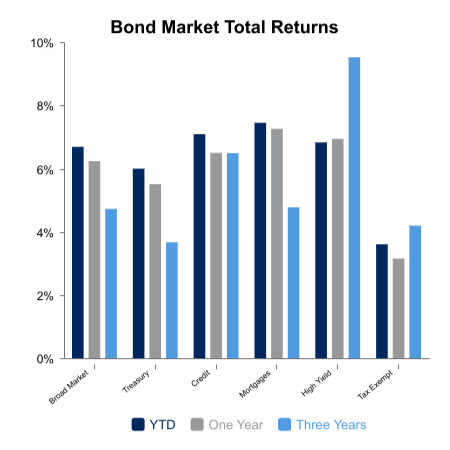

Core bonds were up 0.8% on the week. Yields moved lower as prominent FOMC officials expressed a desire to cut interest rates at the upcoming December meeting. December rate cuts odds have gone from 100% to under 50% to now residing at 80%. This still leaves room for an upside surprise when they likely cut, but markets will be looking for clues that further easing is expected.

The previously highlighted market breadth warning signs triggered a 5% drop in the S&P 500 with weakness centered in the momentum names. Since then, the market has put in some signs of a potential bottom with historically strong 12-month forward returns. These include a 22-to-1 upside to downside day in small caps paired with an 8-to-1 upside to downside in the S&P 500. These followed the previous day where the market registered a high amount of downside selling, which is suggestive of washed-out conditions.

Economic Data Resumes

The economic data has returned, and it’s clear as mud. Delayed September nonfarm payrolls jumped above 100,000 which was an upside surprise. Underneath, however, things appear worse. Manufacturing payrolls have come in negative for five consecutive months. In the last twenty years, this only occurred during recessions. Offsetting this are jobless claims that remain pinned in the low 200,000 area, which is indicative of continued economic expansion.

Consumer confidence is in the dumps but has been for three years as the S&P 500 has risen 95% from its 2022 low. Maybe this is tied to the inflation index, which keeps moving up and to the right despite the rate of change moderating. The 60-month change in the CPI index crossed 25% earlier this year, the last time this occurred was in the early 1970s.

The Atlanta Fed GDPNow is looking for 4.0% real GDP growth for the third quarter. Since the equity market bottom in mid-2022, there have been nine quarters of GDP growth at or above 2.5% with three quarters coming in lower. This has happened amid countless “only in recession” economic data points.

|

|

Sources: BTC Capital Management, Bloomberg

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.