In Support of Market Sentiment

Key Takeaways

- Corporate profitability remains resilient.

- Equity markets take a pause.

- Macro-news from non-government sources.

Corporate profitability remains resilient

Companies have been reporting better‑than‑expected results regarding third‑quarter earnings. According to LSEG, for companies that have reported earnings for the third quarter:

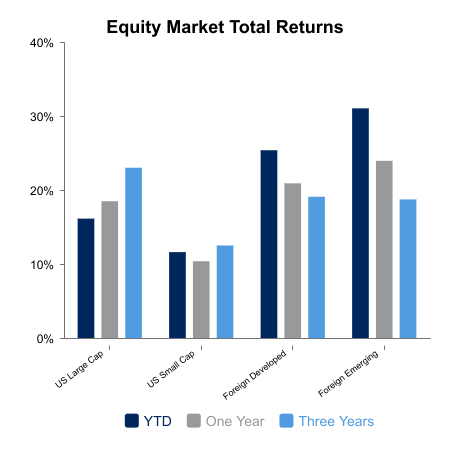

- U.S. large‑cap companies comprising the MSCI USA Index, have reported earnings growth of 17.3% year‑over‑year (YOY).

- U.S. small-cap companies comprising the MSCI USA Small-Cap Index have reported earnings growth of 32.9% YOY.

- Foreign developed companies comprising the MSCI EAFE Index have reported earnings growth of 11.5% YOY.

- Emerging market companies comprising the MSCI Emerging Markets Index have reported earnings growth of 16.7% YOY.

Equity markets take a pause

This past week has seen a pause in equity markets as investors digest a perceived less dovish Fed, concerns about private credit, and ongoing scrutiny of the “AI” trade.

The Russell 3000 Index declined 1.3% for the week. Growth underperformed Value, -2.2% versus -0.3%. Year‑to‑date (YTD) the Russell 3000 is up 16.0%

Outside the U.S., the MSCI All‑Country World ex-USA Index (ACWI ex-USA) fell 2.1%. Similar to the U.S., Growth underperformed Value, -2.5% versus -1.7%. ACWI ex-USA has risen 27.9% YTD.

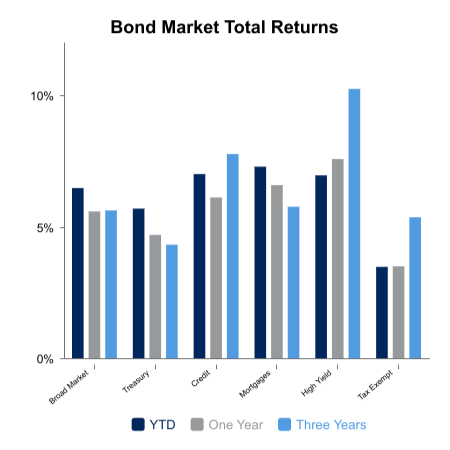

Separately, the yield on the U.S. 10-Year Treasury rose to 4.1% from 3.9% which pushed fixed income returns down 0.5% for the week. Bonds exhibit positive returns of 6.4% YTD.

Macro-news from non-government sources

While the government shutdown has limited data reports, other venues have provided some insight, albeit qualified concerning outlook.

S&P Global, in conjunction with J.P. Morgan, released its Global Composite PMI for October. The Output Index rose to 52.9, up from September’s 52.5 print, achieving a 17‑month high. S&P reported “The start of the final quarter of 2025 saw the rate of expansion in global economic activity accelerate, as growth of new work intakes picked up to a 17-month high. Trends in business sentiment and international trade were less positive in comparison, as optimism eased from September’s recent high and new export business contracted at the quickest pace since July.”

ADP released its Employment Survey for October, reporting private employers added 42,000 jobs. While this was seen as a “rebound from two months of weak hiring”, ADP expressed concerns regarding the lack of breadth of hiring, which seemed to be limited to a few sectors.

The Institute for Supply Management (ISM) reported services PMI for October came in at 52.4, its highest reading since February. This increase was driven by new orders, which rose 5.8%. ISM cautioned concerns exist, specifically regarding the impact of the government shutdown going forward.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., London Stock Exchange Group Plc, FTSE Russell, S&P Global, Inc., ADPResearch, Institute for Supply Management.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.