Equity markets – Higher and Higher

Key Takeaways

- Stocks reach yet another record level.

- Housing market metrics improve.

- Top 10 stocks now constitute over 40% of the S&P 500 Index.

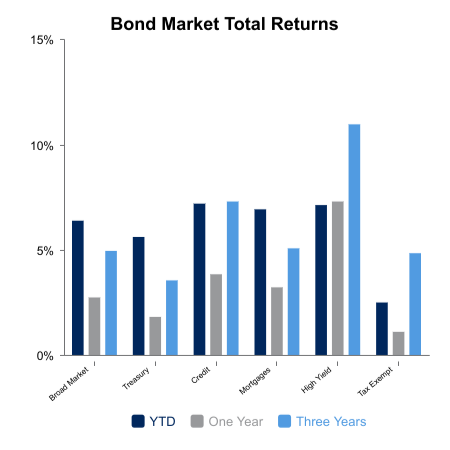

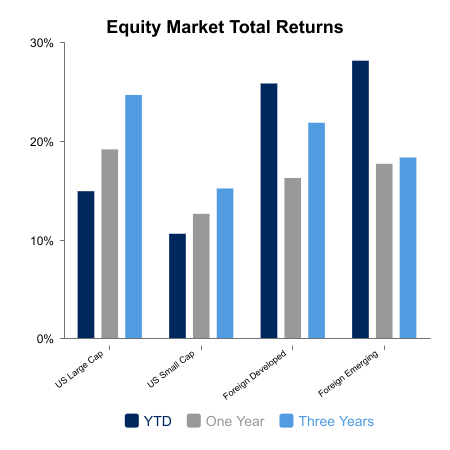

Equity markets rose during the week as investors drove markets to record high levels. Both the S&P 500 Index and the Nasdaq Composite gained 1.1%. The Magnificent 7 rose 0.9%. Small caps climbed 0.7% for the week. Bond indices rose 0.3% during the week.

Strong GDP growth, tame inflation, solid housing market

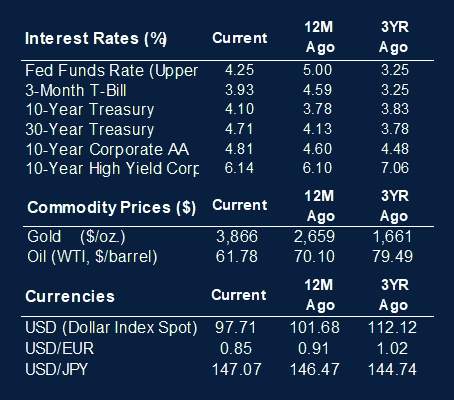

This week saw second quarter GDP revised upward on its final print, rising to 3.8% as an increase in personal consumption and investment led to the upwards revision.

Inflation metrics continue to come in moderately tame, with the latest Core Personal Consumption Expenditures (PCE) reading for August coming in as expected at 2.9% on a year-over-year basis. Despite fears of increasing inflation due to proposed tariffs introduced earlier this year, the U.S. economy has seen only muted rates of inflation. Earlier this week, new proposed tariffs were introduced on select housing products, heavy trucks and upholstered furniture.

Recent employment figures have been mixed. Earlier this month, non-farm payrolls came in much lower than expected. This week, job openings as measured by the JOLTS metric, came in higher than expected and essentially flat from the prior month.

The housing market has seen improvement via various recent economic releases. Pending, existing and new home sales all came in higher than expected for the month of August. With the falling interest rate environment, demand for homes has increased as mortgage rates have moderated.

Upcoming economic releases may be delayed as the Senate failed to pass the continuing resolution for government funding, and as such, many government services, including those responsible for economic data, have been shut down while this matter gets resolved.

Kickoff to third quarter earnings season

Third quarter earnings season will begin soon. Expectations are for year-over-year earnings growth of 8.8%, lower than first and second quarter year-over-year earnings growth rates which saw low double digits. Sectors expected to lead earnings growth include the usual suspect, the Technology sector. However, other sectors such as Industrials and Materials are also expected to lead earnings growth. Calendar year 2025 earnings growth is currently forecasted at 10.8%, while calendar year 2026 earnings growth is currently forecasted at 14.1%.

U.S. sees an uptick in global equity flows

During the third quarter, US stocks outpaced foreign developed markets. Flows into global equities outside the U.S. have been recently trending downward while global flows into U.S. equities have rebounded.

Returning to a more “concentrated” index

With the recent rally within the Magnificent 7 stocks, the S&P 500 is again leaning toward a heavier skewed index. Currently the top 10 stocks in the S&P 500 represent just over 40% of the entire weight in the index. This reverses the trend from earlier in the year when the stock market rally was more broad based.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.